Query

Please provide an overview of existing evidence on undercover integrity testing as an anti-corruption measure, including in the customs sector.

Introduction

This Helpdesk Answer focuses on the effectiveness of undercover integrity testing, an integrity measure in which an organisation simulates an event that places an employee, without their knowledge, in a monitored situation with an opportunity for unethical decision-making (see Davis et al. 2000; ACLEI 2011; Hac 2016; DCAF 2021). For example, one scenario involved placing valuable goods at a simulated crime scene to test whether a law enforcement officer would steal them (ACLEI 2011: 4).

The use of integrity testing in policing can be traced back to the early 1970s when it was employed in the US with the aim of reducing corruption within the New York Police Department (NYPD) (Knapp et al. 1972; DCAF 2021). Integrity testing has since been adopted as an anti-corruption tool in various sectors in many other countries including Australia, Hungary, Romania, Kenya and Moldova.

A study on the border guards and internal affairs units of 27 EU member states, using survey evidence, identified the following methods through which integrity tests can be implemented (Center for the Study of Democracy 2012: 107):

- background/security checks of potential employees

- polygraph tests (lie detector)

- drug and alcohol tests

- monitoring of personal lifestyles, comparing disclosed income with spending, assessment of debt

- random or targeted inspections of officers’ workplace or vehicles, document based inspections, monitoring of officers’ personal/HR files

- offering bribes to officers, creating an opportunity for the officer to become involved in corruption

This indicates that the term integrity testing can be used to describe a wide range of practices. This Helpdesk Answer focuses on integrity testing that has an undercover element and aligns with the widely-used typology that distinguishes between targeted and random tests (ACLEI 2011; Mandić and Đorđević 2016: 12; WCO 2017; DCAF 2021).03d02227b5b2

Random integrity tests involve testing officers who are not under suspicion of corruption or any form of misconduct. The primary goal is to serve as a deterrent to corrupt behaviour (Homel 2002; ACLEI 2011; Hac 2016; DCAF 2021). This type of test can be applied broadly within an organisation or within certain units that exhibit higher risks of corruption (ACLEI 2011: 5).

Targeted integrity tests are directed at specific individuals or groups and are conducted based on previously collected and analysed intelligence (DCAF 2021). Therefore, for a targeted test to occur, there needs to be a trigger, such as an allegation or complaint (ACLEI 2011). They may be conducted as part of a formal criminal investigation related to corruption, depending on the jurisdiction (Prenzler and Ronken 2001; ACLEI 2011: 5).

Hac (2016: 70) additionally categorises both targeted and random tests as either dynamic or static. Dynamic integrity tests involve contact between an undercover officer and the officer being tested, while static tests are carried out without such contact.

An example of a dynamic test would be staging a controlled encounter between an undercover officer and the tested subject; for example, an undercover officer intentionally committing a traffic violation and then observing the traffic officer’s reaction (The Anti-Corruption Bulletin 2020: 15).

Static tests assess the behaviour of tested subjects in situations where they are likely to be alone, such as inspecting break-ins or abandoned vehicles (Hac 2016: 72).

Integrity testing is now used in a number of countries, covering varying sectors with different types of sanctions involved (see Table 1).

Table 1. Integrity testing approaches by country.

|

Country |

Introduced |

Coverage |

Sanctions |

|

USA |

1994 |

police |

disciplinary/criminal |

|

Australia |

1996 |

police |

disciplinary/criminal |

|

UK |

1999 |

mainly police |

disciplinary/criminal |

|

Georgia |

2003 |

public administration |

criminal |

|

Kenya |

2006 |

public administration |

disciplinary/criminal |

|

Czechia |

2009 |

security forces |

disciplinary/criminal |

|

Romania |

2009 |

Ministry of Interior |

disciplinary/criminal |

|

Hungary |

2012 |

public administration |

disciplinary/criminal |

|

Moldova |

2013 |

public administration |

disciplinary |

Source: Ciubotaru no date.

This Helpdesk Answer is structured as follows. The next section focuses on the effectiveness of these tests as an anti-corruption tool. The section after that considers the operational implications of undercover integrity testing. The final section explores the use of undercover integrity testing in the customs sector.

Effectiveness of undercover integrity testing as an anti-corruption tool

Detecting corruption

There is evidence indicating that integrity testing can be effective in achieving one of its main goals – the detection of corruption. For instance, in New South Wales, Australia, targeted integrity testing was introduced to allow for tests on police members in response to intelligence, including complaint patterns (ACLEI 2011).

Their data suggests that out of 90 integrity testing operations conducted between 1996 and 1999, 37% were failed8bbb87c19b13 by the subject officers, 27% passed, 12% forwarded for further investigation and 24% were inconclusive or discontinued (Prenzler and Ronken 2001; ACLEI 2011: 7). Failed tests resulted in 51 criminal charges, of which 54% were against police, 23% against non-police staff and 23% against civilians (ACLEI 2011: 7). The findings indicated that police corruption involves a range of participants beyond police officers, and integrity tests were useful in detecting these groups (Prenzler and Ronken 2001). Criminal charges resulting from integrity testing show a large variation in offences, including assault, embezzlement, possessing prohibited weapons and drugs (Prenzler and Ronken 2001: 330).

In Romania, permission to implement integrity testing was granted to the Anti-Corruption General Directorate (DGA)e5f535dcbecf in 2007. Both random and targeted tests are used and, following failed tests, DGA employees consult with the prosecutor, whose opinion determines the follow-up action (Hac 2016). Between 2007-2010, there were 118 tests for 136 employees, of which 38 (28%) failed, and 31 of these were charged with corruption (Hac 2016: 74).

The National Protective Service of Hungary (NPS) is responsible for integrity testing. NPS is an independent part of the Hungarian police, led by the director-general, appointed by the Minister of Interior (Nagy and Ripszám 2021). Integrity testing covers law enforcement and most of the public administration (The Anti-Corruption Bulletin 2020). In 2022, the NPS carried out 278 integrity tests, resulting in 13 prosecutions (Corruption prevention 2023). Over the last 10 years, there have been 8,830 integrity tests, with 137 leading to criminal or administrative proceedings and 83 resulting in final court judgements (GRECO 2023: 31). The evidence suggests that integrity testing has been effective in uncovering a significant number of petty corruption cases. However, the tests appear to primarily target low-level officials, particularly among border and traffic police (GRECO 2023: 31).

One of the key purposes of integrity testing by the Kenyan Revenue Authority is to test for the risks of bribe demands from KRA officers to clients (Citizen Reporter 2023). A recent undercover operation led to the arrest of one KRA official for demanding a bribe (Klage 2023).

However, subjects of integrity tests may find ways to adapt and avoid detection. In Moldova, the installation of cameras in police cars was used as a preventive measure against integrity violations. However, evidence suggests that police officers tried to ensure the cameras were covered and did not record them taking bribes, including when undercover agents were involved (DCAF 2021: 6) There may be ways to counteract this; for example, in Peru, integrity testing limited to the police was recently introduced using hidden cameras (Ministry of Interior of Peru 2018); if such cameras are well-hidden, the subjects of the test may not be able to tamper with them.

Deterring corrupt behaviour

On a longer term basis, undercover integrity testing also shows promise in deterring corrupt behaviour. The introduction of undercover integrity testing in Moldova in 2014 under the professional integrity testing law was considered by Ciubotaru (no date) to have had a deterrent effect on corrupt behaviour.

The law provides for targeted and random testing applied to all public institutions and was carried out by the members of the National Anti-Corruption Centre (NAC) and the Intelligence and Security Service (ISS) (Ciubotaru no date) pretending to be ordinary citizens applying for public services. Public officials were notified of the measure prior to implementation, and NAC conducted 472 training sessions for public officials on how to respond to bribe offers (Hoppe 2015).

According to Hoppe (2015), the programme had immediate positive effects, including public officials becoming more hesitant to demand bribes (as any citizen could be a potential tester), as well as an increase in reporting bribe offers to public officials, which had the knock-on effect of reducing the number of citizens offering bribes.

In the US, undercover integrity testing in the NYPD is carried out by its Internal Affairs Bureau (IAB).702f45b070c8 The IAB conducted around 500-600 random tests and 25-30 targeted tests annually as of 2016 (Hac 2016: 72). Evidence suggests a strong preventive role of these tests as, after 10 years of implementation, the percentage of people failing the random test was only a few cases per year (Hac 2016). However, some police officers were reportedly affected by the tests and would become paranoid about handling valuables during their work (Hac 2016). This finding suggests that random integrity tests may hinder police officers in the performance of their regular duties if they start to continually fear they are being subjected to such tests.

In the case of Romania, the data between 2011-2013 shows that out of 206 tests involving 239 employees, 16% failed the test, suggesting a decrease in the percentage from the period between 2007-2010, which was 28% of 118 tests conducted on 136 employees (Hac 2016: 74). These numbers may indicate a preventive role of integrity testing in deterring corrupt behaviour in Romania (Hac 2016).

However, there is also some evidence that potentially corrupt subjects may not be deterred but will instead adapt their behaviour. One reported unintended effect of integrity testing in Hungary was that some traffic police started to target more foreign national drivers for bribe extortion as such drivers were considered less likely to be undercover officials (Centre for the Study of Democracy 2012: 118).

Encouraging officials to report bribery

There is evidence indicating integrity testing can incentivise public officials to report bribery.

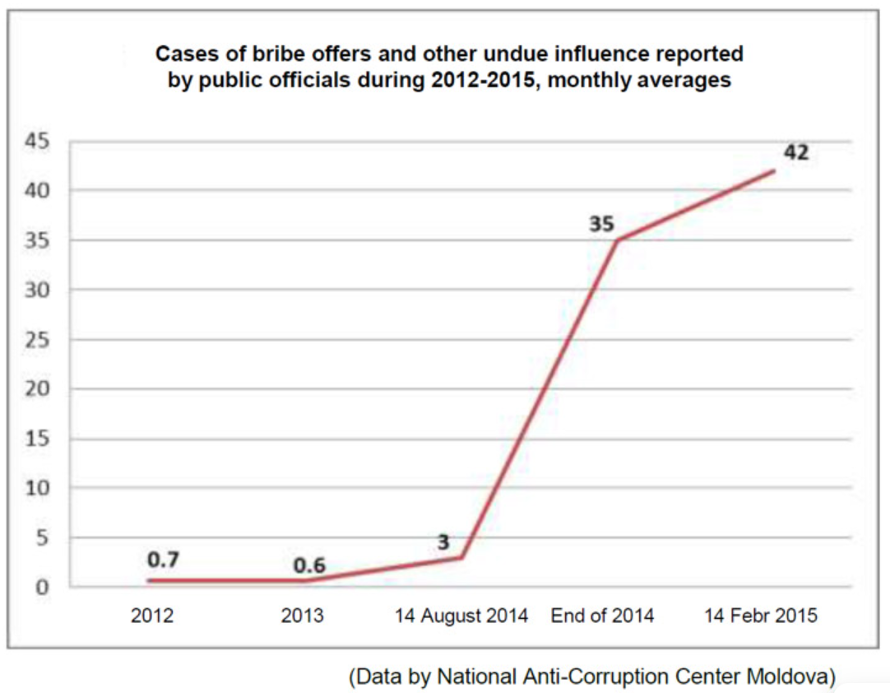

For example, the number of public officials reporting bribe offers and other forms of undue influence surged strikingly soon after integrity testing was introduced in Moldova (Hoppe 2015). It was found that the testing helped break down the “code of silence” in the workplace (DCAF 2021: 5).

Figure 1 shows the average monthly rates. For the total reporting cases in 2014, there were 18 before August (for 7.5 months), while there were 158 after the law came into effect (during the last 4.5 months of 2014) (Ciubotaru no date).

Figure 2. Reported bribe offers and other undue influence on public officials in Moldova before and after the introduction of integrity testing.

Source: Hoppe 2015.

Identifying risks and training needs

Undercover integrity testing targets individuals or a group of employees, but it can have effects at a more organisational level. Since 2012, the task of planning and conducting integrity tests for employees of the police, prison services, and the customs administration in the Czech Republic has been entrusted to the General Inspection of the Security Forces (GIBS) (The Anti-Corruption Bulletin 2020).

The Czech experience shows that integrity testing can be used to identify areas with high corruption, and therefore guide policymaking. Specifically, the results of integrity testing in the Czech Republic showed that the traffic police were disproportionately involved in integrity violations, leading to a broad anti-corruption campaign targeting traffic police (DCAF 2021: 6).

Undercover integrity testing has also been used to identify training needs. For example, integrity testing in New South Wales identified several managerial issues, which led to the implementation of a regional management training programme (DCAF 2021: 6). Integrity testing can also help identify the training requirements of the testing units’ officials. The 1996 KPMG report about the effectiveness of the random testing programme in the NYPD in the US found that the random testing programme was a potentially significant tool in identifying training needs (Davis et al. 2000: 7). At this time, the IAB was regularly submitting training recommendations based on insights from the integrity tests, but there was no system for tracking or recording training needs (Davis et al. 2000: 7). Therefore, KPMG recommended that the IAB should establish standardised forms and official written procedures for documenting training needs arising from the integrity testing programme (Davis et al. 2000: 7). The practice and procedures in the NYPD have evolved over time; those involved in implementing the test need to fill out a form that describes how the test was carried out and provides an opportunity for the subject officer and the testing team to provide feedback (Davis et al. 2000; DCAF 2021).

Identifying employees with integrity

The results of undercover integrity tests have been used to inform decisions on whether officials should be promoted (DCAF 2021).

In the Kenyan case, there is an oversight committee of representatives from the support services department, investigations and enforcement department, human resources department, the KRA integrity division and an official from the Kenya Anti-Corruption Commission (WCO 2017: 39). This committee serves as the integrity review board, determining which officers exhibit high levels of integrity during testing (WCO 2017: 39). Those identified as such are then given preferential access to working on high-profile cases and enjoy an accelerated career development pathway within the KRA (WCO 2017: 39).

Targeted or random tests?

Measuring the efficacy of undercover integrity testing should take account of the different modalities of implementation, and evidence suggests targeted integrity testing has several important advantages over random testing. These advantages include, for example, targeted tests being more sophisticated and thus harder to recognise by the tested subject and being more cost-effective than random tests due to the lower number of subjects (ACLEI 2011; Prenzler and Ronken 2001; DCAF 2021).

In Australia,671965398c35 a 2011 inquiry looked at the advantages and disadvantages of random and targeted tests. Most entities making submissions to the inquiry preferred targeted tests as the random approach was considered to have a negative impact on agency morale and to be less cost-effective (ACLEI 2011). For instance, the integrity commissioner, drawing on evidence from jurisdictions using random testing, stressed that the failure rateis lower in random tests compared to targeted ones (ACLEI 2011: 27). Targeted tests were also favoured over random ones by the Australian Federal Police (AFP) based on their experience implementing both; they found that random testing can have a negative impact on work culture, morale and productivity (ACLEI 2011).

The NYPD uses both random and targeted integrity tests. However, a KPMG report in 1996 found there were inherent difficulties in creating realistic scenarios for random tests (Prenzler and Ronken 2001: 323). According to the report, 355 tests involving 762 officers in a sampled period resulted in no “criminal failures” and merely seven “procedural failures” (Prenzler and Ronken 2001: 323). In contrast, targeted tests resulted in 12 criminal failures and one procedural failure out of 45 tests (Prenzler and Ronken 2001: 323). The report’s conclusion was that random testing largely failed to identify corrupt officers, while targeted testing produced better results because it could tailor scenarios to the profile of suspected officers (Prenzler and Ronken 2001). Nevertheless, the NYPD stressed that the reduction in complaints it experienced could be considered an indicator of the success of both targeted and random tests (Prenzler and Ronken 2001).

Indeed, it should not be considered surprising that the failure rate is higher for targeted tests aimed at suspected officers than for random tests because it is more likely that the officer or a group of officers will repeat the misconduct if they have already been involved in corrupt behaviour (Porter and Prenzler 2012).

Studies indicate that targeted tests are more sophisticated compared to random ones (Homel 2002; DCAF 2021). For example, during integrity testing in the NYPD in 1996, only 3% of random tests were classified as gamma248f112e213b (designating the most complex form of testing), while this figure was 36% for targeted tests (Girgenti et al. 1996). The implication is that, because random tests are less sophisticated, it is easier for officers subjected to random tests to realise that they are being tested and react in a way that they would not have otherwise (DCAF 2021: 8).

Targeted tests are reportedly more effective as test subjects are more likely to recognise the test stimuli (e.g. drugs, cash, property) than those in random test settings (Girgenti et al. 1996). If officers are not made aware of the test stimuli, they cannot be meaningfully tested for corrupt behaviour (DCAF 2021).

Despite these apparent advantages of targeted tests, existing studies, such as Davis et al. (2000) on integrity testing in the NYPD, suggest that it is important to take into consideration the context and specific needs when choosing the type of undercover integrity testing. For example, if there is the challenge of a widespread culture of petty corruption in a particular part of a sector, introducing random testing may act as a deterrent to corrupt practices. Moreover, there is room for a middle-ground solution, such as keeping random testing but focusing it on specific units within an organisation that display high corruption risks. In this case, testing remains random, but the tests can be better tailored, informed by the analysis and evidence of corruption risks in a specific unit.

Operational implications of undercover integrity testing programmes

Before designing and implementing undercover integrity testing programmes, it is essential to consider several operational implications.

Legal issues

There are several legal questions arising from undercover integrity testing that can compromise the admissibility of evidence secured from the test in a court of law or disciplinary proceedings. Nevertheless, countries have introduced legal amendments and safeguards to address these. For example, in New South Wales, the Royal Commission recommended the introduction of legislation on integrity testing to avoid legal issues, and amendments were introduced in a number of police acts and the drug misuse and trafficking act (Prenzler and Ronken 2001: 328). This was done to authorise integrity tests and protect actors administering integrity tests from facing legal action (Prenzler and Ronken 2001).

While it may differ significantly between national jurisdictions, some common issues are described here. Integrity tests can potentially breach privacy rights and the constitutional safeguards enjoyed by individuals (Sambei and Allen no date; Mandić and Đorđević 2016). In Moldova, certain provisions of the professional integrity testing law were declared unconstitutional in 2015 by the constitutional court (Ciubotaru no date; Šakočius 2021). In 2014, a group of Moldovan parliament deputies had addressed the constitutional court, seeking clarification on the use of the law to test representatives of judicial authorities (Šakočius 2021: 307). The court found that the provisions of the law governing the initiation of testing procedures did not meet criteria for reasonableness and objectiveness, failed to ensure the upholding of the presumption of innocence, and thus were unconstitutional (Šakočius 2021: 307). Therefore, the law was amended in 2016 to address these concerns. Given that this law was the subject of extensive legal analysis with regard to its compliance with human rights standards, it can offer valuable lessons for other countries in preventing threats to the freedoms and rights of civil servants arising from undercover integrity testing (Šakočius 2021: 302).

Another legal issue often associated with undercover measures is entrapment.c46f66066098 The Australian Federal Police (AFP) acknowledged that “entrapment could arise in an integrity testing context if the test was conducted in a way that was likely to induce the subject to engage in unethical, corrupt or criminal behaviour that he or she would not otherwise have intended to commit” (ACLEI 2011: 6).

Nevertheless, the AFP set out elements of the legislative and administrative framework that it believed could address entrapment concerns, including the use of a threshold test based on the degree of suspected criminal activity (ACLEI 2011: 32). Furthermore, to avoid a situation of entrapment, the actors working undercover involved in the test should not overly urge, harass or overly encourage the subject of the test to commit the crime (Justia no date).

In Romania, until 2011, integrity testing was conducted based on secret orders from the minister of internal affairs. However, this approach faced criticism during the Romanian EU integration process due to its lack of transparency and potential for misuse (Mandić and Đorđević 2016: 28). As a result, the practice changed, with the enactment of legislation in 2011 to strengthen oversight over operations and enable public access to the testing methodology (The Anti-Corruption Bulletin 2020; Mandić and Đorđević 2016: 28). The legislation also stipulated that it is forbidden to provoke the tested person to commit misdemeanour or criminal offences (The Anti-Corruption Bulletin 2020; Mandić and Đorđević 2016). Moreover, every aspect related to the organisation and conduct of integrity testing is now recorded in a document titled “Plan for professional integrity testing”, which includes information on the personnel category to be tested, the participants, versions and backups of the activities, technical and other details (The Anti-Corruption Bulletin 2020: 27).

Similarly, in Hungary, integrity measures must be implemented in line with legal safeguards. After an amendment to the police act came into effect in 2021, integrity testing can target all staff under the supervision of government and its members, with the exception of the ministry of defence (GRECO 2023: 31). The prosecutor has to be informed about both the order and completion of integrity testing. In the case of the order, a detailed plan needs to be submitted, based on which, the prosecutor decides whether to approve the testing within two working days (The Anti-Corruption Bulletin 2020: 17). The grounds for ordering a test do not have to be based on intelligence on an individual officer but can be based on high corruption risks associated with a specific job (Nagy and Ripszám 2021: 68). However, the freedom of choice of the tested subject cannot be compromised, and they must not be coerced into accepting the offer (Corruption prevention 2023).

In the context of the Council of Europe, Sambei and Allen (no date) recommended that integrity testing is accompanied by several safeguards, including:

- there is a legal basis for conducting the test and all necessary authorisations are in place

- all stages of the tests (including preparation) should be properly recorded

- it is treated as an investigatory method of last resort, to be relied upon only when other measures have been exhausted

- the use of testing is proportionate to the misconduct being investigated

- prosecutors should assist investigators in formulating a strategy and providing advice on the test, with regards to its feasibility, credibility, and legal issues

Lastly, it is worth noting that different approaches exist across jurisdictions regarding the regulation of who is responsible for administering integrity testing programmes. While this is normally specialised agencies or law enforcement units (Šakočius 2021), such powers may also be delegated through legislation.

Since 2012, Australia has strengthened the anti-corruption powers of the Australian Customs and Border Protection Service (ACBPS), with the legislation enabling them to conduct integrity testing of customs and border protection officers (Grant 2013). In Moldova, the National Anti-Corruption Centre (NAC) and Intelligence and Security Service have the authority to conduct integrity testing (Ciubotaru no date). In Czechia, the General Inspection of the Security Forces (GIBS) is responsible for integrity testing in police, prisons and customs services (Mandić and Đorđević 2016). The employees of the inspection have police powers and can initiate an integrity test by submitting a request to the prosecutor’s office for approval (Mandić and Đorđević 2016: 24).

Resources

As integrity tests require creating detailed and realistic scenarios, preparing a test can be a costly endeavour (ACLEI 2011). This is particularly relevant for random tests, which tend to be more expensive than targeted ones due to their wider scope (Faull 2009; DCAF 2021). A KPMG report in 1996 concluded that any benefits accrued by NYPD through the use random testing did not justify the associated costs.

These costs include training staff and purchasing equipment to ensure the testing is carried out effectively. For example, the NYPD’s efforts to save evidence in both random and targeted tests were frequently impeded by the failure to record the test with audio or video, or because of technical issues with recording devices (Davis et al. 2000: 3). Critics of integrity testing often highlight that, because of their extended duration and costly equipment, these tests divert resources from an organisation’s primary functions (Goldsmith 2001).

Considering the effectiveness of undercover integrity testing as an anti-corruption measure, options can be considered to make testing more cost-efficient (Homel 2002) rather than to avoid using the measure altogether. For example, the Mollen Commission4a1962704642 recommended that the Internal Affairs Bureau (IAB) of the NYPD conduct random tests based on a corruption risk assessment, targeting police units facing higher risks (Davis et al. 2000: 3-4).

Employee morale

Integrity testing risks damaging employee morale, as subjecting officers to integrity tests can result in them feeling that they are under constant surveillance and do not have the freedom to perform their duties without fear (Mandić and Đorđević 2016).

ACLEI (2011) found there was some evidence to suggest that random tests can negatively affect the morale of an organisation, including the erosion of the trust relationship between employer and the employee, as well as undercutting the readiness of public officials to act with confidence, particularly in roles requiring fast judgement.

The Western Australia Police made a distinction between day-to-day morale and agency esprit de corps (ACLEI 2011: 14). Namely, they pointed out that, although random testing may initially be perceived by officers as an infringement, it will ultimately be judged on whether it effectively targets (even randomly) those high risk areas (ACLEI 2011: 14). Their expectation was that, having integrity testing in the workplace could affect day-to-day morale but commitment to the organisation and the profession, known as esprit de corps, would remain unchanged (ACLEI 2011: 14).

Indeed, the subjects of integrity testing may view it as a necessary measure to root out internal corruption. Miller (2010) carried out an attitudinal study of Victoria Police officers, finding a generally high acceptance of targeted integrity testing among them.

Undercover integrity testing in the customs sector

This section considers the use of undercover integrity testing in the customs sector.

The Revised Kyoto Convention defines customs “as the government service responsible for the administration of customs law and the collection of taxes and duties and which also has responsibility for the application of other laws and regulations related to the import, export, movement, or storage of goods” (WCO 2008a).

Customs administrations are particularly vulnerable to corruption and are frequently cited as among the most corrupt government agencies (McLinden 2005). For example, a 2015 report revealed that the US Customs and Border Protection Agency had the highest number of law enforcement officers arrested for corruption per capita compared to other federal law enforcement agencies in the US (Homeland Security Advisory Council 2015: 6; Bennett 2015).

The WCO members (2003 no date) have expressed a commitment to tackle integrity challenges in the customs sector. For example, the Revised Arusha Declaration identifies 10 areas5fb661d11370 that effective national customs integrity programmes should consider enhancing.

In some jurisdictions, law enforcement authorities or customs administrations have the power to conduct undercover integrity testing on customs officials, including Australia and Moldova. As with other sectors, there is evidence it can be effective in customs; following the introduction of testing in Moldova in 2014, the most reports by public officials of corruption and undue influence attempts came from the customs service, as shown in Table 2.

Table 2. Reported bribe offers and other undue influence by public officials in different institutions in Moldova in 2014.

|

Institution |

Reported bribe offers |

|

Customs service |

59 |

|

Ministry of Interior |

41 |

|

Ministry of Justice’s Civil Registration Offices |

19 |

|

NAC |

17 |

|

Health care institutions |

6 |

|

Courts of law |

6 |

|

Mayor’s offices |

5 |

|

Other entities |

23 |

While the literature on the application of the undercover integrity measures in the customs sector is not extensive, certain benefits can be hypothesised based on the characteristics of the sector.

There are several factors contributing to corruption in the customs sector, including the monopoly power of customs officials over clients, discretionary powers of customs employees over the provision of goods and services, and often low levels of control or accountability (WCO 2021: 14). Other factors that facilitate corruption in the customs sector include customs officials often working in remote and unsupervised border stations and the time-sensitive nature of many types of goods (WCO 2021: 15). Corruption identified in the customs sector can be categorised into collusive and abusive practices (Ardigó 2014: 8). The former involves cases of importers and exporters colluding with customs officials to evade duties or inspection of goods, for example, while the latter refers to practices such as bribe extortion by officials or embezzlement of revenue (Ardigó 2014: 8).

Undercover integrity testing could effectively recreate some of the typical scenarios of corrupt behaviour within the customs administration and target officials’ discretionary power. For instance, designing and implementing an undercover integrity test to simulate the scenario of offering bribes to customs officials can be easily accomplished. As established in previous sections, this can lead to both the detection and deterrence of corrupt practices, and thus address any gaps in control or accountability.

Nevertheless, the operational implications of undercover integrity testing must also be applied to the customs sector. Importantly, depending on the local jurisdiction, customs administrations may encounter legal issues if they attempt to implement undercover integrity testing, meaning prior consultations with relevant actors such as public prosecutors is essential.

The associated costs of implementing undercover integrity testing must also be considered; these may be higher if the subjects are remotely located customs officials. Furthermore, in some parts of the world, customs officials already experience poor working conditions and low salaries, which also serve as incentives for corrupt behaviour (Walsh 2003: 160). Therefore, before implementing integrity testing programmes in customs administration, it is imperative to conduct a cost assessment to determine whether the resources allocated for the development, implementation and maintenance of undercover integrity testing programmes would have a detrimental effect on the working conditions and salaries of customs administration officers.

Another significant operational implication to consider is the potential negative effect on the morale of customs officials. Employment in customs administration is often viewed as a short-term opportunity, rather than a long-term professional career (Walsh 2003: 156). According to Walsh, there may be limited loyalty to the organisation, as officials see limited prospects for career advancement (Walsh 2003: 159). A decision to implement undercover integrity testing should take account of the risk that the measure will be unpopular if morale levels are already low. One possible countermeasure to explore in this regard would be the application of undercover integrity testing towards outcomes that more directly benefit staff, such as enhanced training and the identification of candidates for promotion opportunities.

- Some authors (Sambei and Allen no date) use different terminology to distinguish between various types of integrity tests, categorising them as random virtue tests and intelligence led tests, which align with the aforementioned distinction between random and targeted tests.

- In the context of integrity testing, failure indicates that the tested subject engaged in or reciprocated the simulated corrupt or unethical act and consequently did not pass the integrity test.

- DGA was established as a separate institution in 2005 with the authority to prevent and counter corruption among personnel reporting to the Ministry of Internal Affairs (including police, border guard, gendarmerie and fire brigade) (Hac 2016). Since 2013, the DGA has been part of the Ministry of Internal Affairs(Hac 2016).

- Over time, a specialised unit for devising the concept of testing, implementation and analysis of their impact, as well as for transferring materials for further official or criminal use, was created within the IAB (Hac 2016: 71).

- In 2012, the Australian Parliament passed legislation that strengthened anti-corruption powers of the Australian Customs and Border Protection Service (ACBPS). These powers, among others, included the ability to conduct integrity testing of customs and border protection officers (Grant 2013).

- Both random and targeted integrity tests are divided into three levels of complexity: alpha, meaning least complex, beta, meaning middle-level complexity, and gamma, referring to most complex (Girgenti et al. 1996: 4).

- Entrapment has been defined as “an affirmative defense in which a defendant alleges that a law enforcement agent or agent of the state acquired the evidence necessary to commence prosecution of the defendant by inducing the defendant to engage in a criminal act that the defendant would not otherwise have committed” (Legal Information Institute 2022).

- The commission to investigate allegations of police corruption and the anti-corruption procedures of the police department.

- These include leadership and commitment, regulatory framework, transparency, automation, reform and modernisation, audit and investigation, code of conduct, human resource management, morale and organisational culture, and relationship with the private sector (WCO no date).