Engaging on anti-corruption in a constrained multilateral landscape

Multilateral organisations remain central to delivering Official Development Assistance (ODA). In 2024, global ODA fell by 7.1%,d3c8cc456be1 with further reductions expected in 2025, especially following the US withdrawal from several multilateral initiatives.7fa18b2b9f95 Declining core funding and increased reliance on earmarked contributions have intensified pressure on multilaterals to demonstrate transparency and efficiency, even as their resources shrink.

The multilateral system has also grown more complex. The number of ODA-eligible organisations increased from 121 in 2000 to 212 in 2020. Meanwhile, the share of development finance channelled through them rose from 45% in 2010 to 61% in 2022.43ffab0aadb0 This expansion has fragmented oversight, complicating accountability. Yet multilaterals still channel about one-third of total ODA, or two-fifths if earmarked contributions are included, despite persistent governance challenges.

In this context, robust corruption risk management is more urgent than ever. Diversion of limited resources can undermine public support, disrupt operations, and damage the credibility of multilateral cooperation. However, current safeguards remain uneven. A 2023 Joint Inspection Unit review highlighted the limited integration of anti-corruption provisions across UN organisations.368dfae5313c

U4 partners06bac5ae9906 identify two key challenges. First, donors struggle to influence multilateral anti-corruption practices. Second, they often lack reliable information on corruption risks. Donors themselves contribute to fragmentation by using earmarked contributions, trust funds, and vertical initiatives, which weaken oversight and reduces leverage for stronger safeguards.

Efforts to strengthen donor influence often face political resistance. Recipient countries and multilateral bureaucracies may view anti-corruption demands as threats to organisational independence. Donors must balance their desire for greater integrity safeguards with the need to preserve the legitimacy and neutrality of multilateral institutions. This dilemma is exacerbated by declining public trustfbca0f3f9627 and intensifying geopolitical fragmentation.339cff8b7673

Despite these challenges, there is an opportunity. Multilaterals, seeking to retain donor confidence amid funding cuts, may be more open to transparency and reform. A critical entry point is anti-corruption requirements in donor–multilateral framework agreements. These agreements are more than financial instruments. They define the reporting and accountability conditions governing entire donor portfolios. By shaping how organisations operationalise integrity safeguards, they offer a strategic lens to assess coherence, robustness, and harmonisation.

The analysis reviews framework agreements across major donors, supplemented by interviews and case material. It also draws lessons from reforms on sexual exploitation and abuse (SEA), showing how coordinated donor action in another sensitive area has shaped multilateral oversight. This precedent is not the focus of the study, but it provides an illustrative benchmark for the anti-corruption agenda developed here.

Our study examines the design of current anti-corruption safeguards, identifies gaps, and proposes options to strengthen collective donor leverage. Yet framework agreements have limitations. They are often aspirational and do not capture day-to-day implementation. However, they reveal systemic strengths and weaknesses in donor oversight. They also highlight where collective action could reinforce accountability. This dual perspective sets the stage for the analysis that follows.

Methodology

This analysis is based on desk research, including a review of framework agreements between U4 partner agencies and United Nations organisations. The focus is on anti-corruption requirements: the minimum institutional safeguards, disclosure obligations, and integrity measures expected by donors.

For some donors, we were provided with the framework agreement templates that apply to all UN agencies. For others, we had access only to the anti-corruption provisions included in all their agreements. In a few cases, the material covered specific agreements with key UN agencies (UNDP, UNICEF, UNOPS, WFP, UNHCR, and UN Women).

In total, the review covered 40 agreements and templates across eight donors. When donors maintain multiple agreements with a single organisation (for example, Norway), we were given the most recent and financially most significant ones. The agreements analysed were signed between 2020 and 2025. At the request of participating donors, the framework agreements reviewed for this study are treated as confidential documents and are therefore not cited directly in the text.

The study focuses on the shared baseline requirements that recur across agreements and that donors consistently include in their contracts with UN partners. Attention was also paid to the gaps and divergences between agreements, to highlight where certain safeguards appear systematically and where they are absent or unevenly applied.

To complement the desk research, we conducted 14 interviews between September 2024 and March 2025. Participants included donor staff responsible for multilateral relations from U4 partners, and relevant officers from UN agencies. We used remote interviews and anonymised the data to safeguard confidentiality.

The paper first assesses existing anti-corruption requirements in framework agreements, showing strengths, gaps and possible improvements. Second, it reviews capacities and opportunities for donor coordination, providing a clear pathway for change. To provide context, the study also reviews the SEA reform process as a comparative case of donor-driven change in multilateral oversight. This case serves as a precedent that helps frame possible pathways for anti-corruption reforms. Finally, Annex 1 provides a draft template for framework agreements.

Existing provisions and pathways to stronger safeguards

Framework agreements between bilateral donors and multilateral organisations have made important advances in embedding anti-corruption safeguards. All agreements now affirm a commitment to zero tolerance for corruption. They oblige agencies to act on credible allegations and maintain rules on staff conduct, procurement integrity, and whistleblowing protection. This is a marked improvement compared to earlier agreements where such provisions were uneven or absent.

There is also significant convergence across agreements. Most rely on internal oversight bodies to investigate allegations, require agencies to maintain fraud reporting channels, and establish procedures to recover misused funds. These shared elements reflect a broad consensus that safeguarding integrity is central to sustaining donor confidence in the multilateral system.

Divergences are visible in donor attitudes. Some donors approach multilateral organisations almost as contractors with direct liabilities, while others treat them as collective partners where risks are managed jointly. Denmark, Germany, and Norway adopt a prescriptive style, spelling out reporting requirements, audit modalities, and repayment conditions in explicit detail. By contrast, the United Kingdom rely more heavily on agencies’ internal rules, granting them wider discretion. In effect, prescriptive clauses keep stronger control in donors’ hands, while trust-based clauses place greater responsibility on the multilateral system.

Beyond these differences in approaches, provisions vary considerably in scope and detail. Canada’s agreements, for example, set out expectations explicitly and reference oversight and anti-fraud policies in detail. Others, such as Switzerland’s or Sweden’s, use more general language, signalling trust in UN systems rather than stipulating precise provisions. As one UN oversight official noted, ‘Framework agreements vary so much. Sometimes the clauses are broad, sometimes too narrow. There’s no consistency’.

The table below captures these divergences systematically. Each agreement was reviewed clause by clause and coded across five access areas: financial information, fraud reporting, monitoring and evaluation, site access, and repayment modalities. To ensure comparability, terminology was harmonised. Provisions highlighted in green indicate good practices among donors. Each access area will then be developed further, explaining why it matters, mapping existing provisions, and presenting possible improvements.

Table 1. Donor provisions: comparison between U4 partners

| Country | Financial information | Fraud reporting | Monitoring & evaluation | Site access |

Repayment modalities

|

| Canada | UN Standard | UN Standard | UN procedures | Not specified |

Conditional refund / reprogramme

|

| Denmark | UN Standard | Early notification | Donor-led allowed | Donor site access allowed |

Handled under UN rules

|

| Finland | UN Standard + Detailed, result linked financial report | UN Standard | Donor-led allowed | Donor site access allowed |

Conditional refund / reprogramme

|

| Germany | UN Standard + UN Standard partner list | UN Standard | Influence scope of UN-led evaluation | Not specified | Explicit refund |

| Norway | UN Standard + risk information | UN Standard | Donor-led allowed | Donor site access allowed | Explicit refund |

| United Kingdom | UN Standard + structured risk information | UN Standard | Not specified | Not specified |

Handled under UN rules

|

| Sweden | UN Standard+ allocations by subprogramme | UN Standard | Participate in UN evaluation | Via UN evaluation |

Handled under UN rules

|

| Switzerland | UN Standard | UN Standard | Participate in UN evaluation | Not specified |

Handled under UN rules

|

Source: developed by the author.

Financial information

Oversight information is essential for donors to verify how funds are spent, ensure resources are used as intended, and detect risks such as inflated costs, delayed disbursements, or unexplained transfers. Without detailed and timely reporting, donors cannot trace fund flows or assess value for money. This leaves critical gaps in accountability and anti-corruption safeguards.

Access to this information is shaped above all by the single audit principle (SAP). This rule prevents donors from commissioning their own audits and obliges them to rely on the organisation’s internal oversight arrangements. UN policy guidance confirms that agencies 'normally decline to let donors or their auditors have access to accounting records' and 'refuse requests for special audits of individual activities'.b3c89c99fd15 As a result, internal audit reports become the only realistic channel through which donors can verify whether organisational controls work, risks are managed, and corrective measures are taken.

In practice, access to oversight information remains uneven. Some donors secure detailed financial statements with risk-related analysis, while others must rely on aggregated accounts and broad summaries that offer little insight into vulnerabilities. This creates unequal conditions for oversight: some donors can identify risks and hold partners to account, while others depend on system-wide reports with limited diagnostic value.

Two donors stand out for securing particularly detailed oversight. Finland requires reporting that links expenditures to budget lines, results, and risk factors, enabling close tracing of contributions. The United Kingdom negotiated provisional uncertified financial statements and delivery chain risk mapping. In one agreement, the UK also secured the possibility to get specialised financial reporting, a paid option to get more granular financial data and better risk visibility on UN partners.

Other donors have introduced notable but more limited improvements. Some Swedish agreements require disclosure of financial data on how contributions are allocated by sub-programme (for example climate change, environmental governance). Norway requires allocations across result areas in programme documents and risk descriptions in project design. Germany mirrors a strict SAP application at project level, with certified annual financial statements and without risk-mapping or sub-programme breakdowns, but requests implementing-partner disclosure to verify that no partner is under sanctions-list.

Other donors, such as Denmark, Canada and Switzerland, receive certified annual statements that confirm accuracy but offer little activity-level detail. As one Danish officer put it, 'the reports are often very aggregated. They do not show you how the money is actually used on the ground, so it is very hard to trace fund flows or identify problems early on'. A Finnish colleague, reflecting on the UNOPS investment scandal,dc865c097314 added 'third-party audit, like the KPMG report, gave much more accurate information about the situation than all internal reports we received earlier'.

Possible improvement

By negotiating for comparable access across agreements, donors could move towards a more consistent baseline that strengthens accountability and helps detect corruption. To address this, framework agreements could introduce standardised requirements for granular reporting. Reports should link expenditures to results, disaggregates data by activity lines, and clarify the use of earmarked contributions. Such provisions would reduce inconsistencies across agreements and provide a more reliable basis for collective monitoring of financial integrity.

At a minimum, this should include financial risk reports highlighting vulnerabilities in partner selection, fiduciary safeguards, or budgetary controls. The experience of the United Kingdom shows that such access can be negotiated without undermining the principle of a single audit. It also provides donors with a more granular understanding of systemic weaknesses.

To make this access meaningful, reporting requirements should also address usability. Audit material must be structured in a way that allows donor staff to distinguish priority risks without being overwhelmed by volume. Together, these reforms would strengthen early risk detection, improve donor trust, and foster collective accountability.

Fraud reporting procedures

Fraud reporting is central to donor oversight. Timely and reliable alerts enable donors to coordinate responses, protect funds at risk, and identify systemic weaknesses across programmes. Without early notification, donors cannot suspend disbursements, adjust risk management, or align investigations with other partners.

Under current framework agreements, UN agencies reserve the right to review fraud allegations internally before notifying donors. Agencies justify this approach by pointing to the need to protect confidentiality, uphold due process, and shield whistleblowers or other stakeholders. While sensible, these safeguards mean that donors often receive information late or in a filtered form.

Denmark has recently secured stronger provisions that require agencies to notify it of credible fraud allegations. However, these provisions are not automatic. The agency must first determine that the case carries 'significant impact' for its partnership with Denmark, and disclosure remains subject to confidentiality rules. This is a departure from the standard approach and gives Denmark earlier access to information, but the discretion retained by agencies means that alerts can still be partial or delayed. For other donors, notification usually comes later, only once allegations are substantiated or an investigation has formally begun, rather than at first suspicion.

For donors, this creates uncertainty about the timeliness and reliability of alerts. It also reduces their capacity to coordinate responses with other partners, identify patterns that might reveal systemic vulnerabilities, and adapt their own safeguards until well after risks have materialised. As a senior officer from the Swiss cooperation noted: 'Some UN organisations will inform us, but will only share very limited information on the case and how it is being or has been handled. As such, we as donor do not have the necessary information to assess whether the follow-up has been adequate'.

From the UN perspective, disclosure of fraud information is governed both by applicable legal frameworks and by core investigative principles. These are designed to protect confidentiality and due process, ensure witness safety, and avoid compromising ongoing investigations. Access is defined through legal agreements, agency policy frameworks, and the UN’s single audit principle. UN agencies must therefore ensure that any disclosure complies with these requirements while safeguarding the integrity of investigations. Even within this tightly regulated framework, meeting donor expectations places heavy demands on resources. As one UN Director of Investigations explained:

'We have now had to shift resources from those doing investigations over to managing donor relations. About 5–8% of our investigative capacity has been reallocated, and that further slows down the process. Every project has multiple donors, so one case can generate six separate donor calls several times a year. We currently manage around 900 cases, do the math'

This illustrates the structural dilemma: donors request timely information to protect their fiduciary interests, but oversight offices must respond within strict legal and confidentiality safeguards, while also managing the resource diversion this entails. The trade-off underscores the need for harmonised notification protocols that satisfy donors’ expectations while allowing investigative offices to preserve their core mandate.

Possible improvement

Denmark’s new provisions show that framework agreements can be adjusted to give donors earlier access to fraud information, even if disclosure remains subject to confidentiality safeguards and thresholds such as 'significant impact'. This creates a benchmark for other donors, who could work together to secure similar clauses to ensure more consistent access.

To be effective, notification requirements should focus on timely alerts whenever credible allegations present substantial fiduciary or reputational risks. Such measures would need to respect the legal agreements already in place, the UN’s single audit principle, and the safeguards designed to protect confidentiality, whistleblowers, and due process.

Recent steps, such as UNICEF’s new Policy on disclosure of integrity-related information (2025) indicate that agencies themselves are willing to move in this direction. The new policy allows 'Significant Impact Events' to be shared with donors as soon as allegations are deemed credible, while other fraud and corruption cases are reported on a semi-annual basis. Donors are informed of the type of misconduct (fraud, corruption, or sexual exploitation and abuse), the link to their funding, whether the case meets the 'significant impact' threshold, and later, the outcome and remedial actions taken.

While mainly process-oriented to protect ongoing investigations and stakeholders, UNICEF’s new policy marks important progress towards greater transparency with donors. For donors, the policy provides earlier and more structured access to information, which enhances their ability to coordinate with partners and strengthen safeguards before risks escalate. This move could be replicated by other UN agencies and reflected in existing framework agreements to promote greater consistency across the system.

Fraud reporting could also reflect gender-sensitive risk assessments. Misconduct affects women and marginalised groups in particular ways, such as extortion, sexual corruption, or barriers to safe reporting. Tracking cases with disaggregated data would improve detection and strengthen safeguards where vulnerabilities are greatest.

Evaluation rights

Independent evaluations give donors a direct way to check whether multilateral partners deliver results and apply their safeguards in practice. They also help identify lessons learned and systemic weaknesses that do not always appear in routine reporting. However, practice and requests for third-party monitoring can diverge from framework agreements. In the UK case, for example, such requirements are not stipulated in agreements, although they can happen in practice, both in pooled and earmarked funds.

Most framework agreements delegate evaluation responsibilities exclusively to the multilateral agency. Donors receive the reports that agencies decide to produce, but usually cannot commission or initiate independent reviews. For example, several Norway–UN and Sweden–UN agreements assign evaluation functions entirely to the agencies, leaving donors with outputs that are often broad in scope and limited in detail.

Denmark’s recent agreements explicitly allow the Ministry to initiate its own reviews and evaluations to assess project implementation, management, financial integrity, and risks. These reviews are distinct from UN-led evaluations and do not amount to an audit, yet they go further than what most other donors currently have, even if they remain subject to UN regulations and procedures.

Finland and Norway also demonstrate that there is some leeway. In certain agreements, they may lead an evaluation, but only on an ad hoc basis and subject to agency approval. Those possibilities show that the model is not entirely rigid and that space exists to negotiate broader rights. Germany also provides a good example, allowing influence over the scope, timing, and methodology of evaluations, even if those evaluations remain UN-led.

Respondents confirmed existing weaknesses. One observed that 'in some country offices there is limited oversight in the assessment and mitigation actions or even non-existent', raising doubts about whether evaluations are sufficiently targeted. Donors’ own limitations add to the problem. Another respondent noted: 'Most donors don’t have sufficient capacity at all levels to be able to properly monitor and hold these agencies accountable. And there is a culture that says, "we trust these bodies, after all, they are the UN"'.

In practice, evaluation rights remain weak. Donors without access are left entirely dependent on agency-led narratives. Even Switzerland, with limited participation, cannot ensure that evaluations address its most pressing concerns.

Possible improvement

As current arrangements rely mainly on agency-led evaluations, framework agreements could at least guarantee donors structured opportunities to contribute to the design, timing, and methodology of evaluations, without compromising independence. Denmark’s clause shows that stronger donor-led rights can be negotiated within the UN’s regulatory framework, and making such provisions more widely available would reduce asymmetries across donors. For projects of significant financial value or in high-risk contexts, donors could lead an evaluation with the partner’s approval. Mandatory independent third-party evaluations could be introduced, with results disclosed publicly to reinforce accountability and trust.

Site access provisions

Field access is an essential complement to desk-based oversight. Site visits enable donors to verify whether reported results match actual implementation, observe fiduciary and procurement practices in context, and detect risks that rarely surface in written reports.

Among U4 partners, Denmark, Finland, and Norway’s agreements stand out by granting explicit rights to conduct site visits or field verifications in some of their agreements. While these rights remain subject to the agency’s internal regulations and procedures, they nevertheless demonstrate that stronger access provisions can be negotiated. Sweden has a more limited option, allowing site access only when participating in UN-led evaluation missions. For other donors, framework agreements make no provision for independent verification through field missions.

Without these steps, verification rights remain fragmented, limiting donors’ ability to follow up independently on performance concerns and weakening incentives for agencies to address integrity risks across country offices.

Possible improvement

Donors could align with Denmark, Finland and Norway by securing explicit rights to conduct site visits and field verifications. This would ensure consistent access and support accountability.

Repayment modalities

Repayment modalities determine what happens after confirmed wrongdoing or the recovery of misused funds. They are a core element of donor oversight, defining who ultimately bears the financial risk of fraud, corruption, or other irregularities. If modalities are strict, donors can demand that unspent or misused funds are returned. If they are more flexible, funds may instead be reallocated to another activity, or the organisation itself may decide how to manage the recovery internally. The design of these clauses is therefore not a technical detail but a reflection of how responsibility for corruption risks is shared between donors and multilateral organisations.

The agreements show wide variation. Germany and Norway adopt the strictest stance, with explicit clauses requiring repayment of both unspent and misused funds. Canada and Finland represent an intermediate model, consulting donors once funds are recovered and allowing agreement on refund or reprogramming. By contrast, the United Kingdom, Sweden, Switzerland and Denmark defer to multilateral organisations’ own rules, handling recovery internally without giving donors a contractual right to repayment. All donors share a zero-tolerance principle on corruption, but the extent to which they retain control over financial remedies varies significantly.

These divergences affect collective donor leverage. In joint initiatives, some donors may expect cash repayment while others accept reallocation, creating asymmetry in how agencies respond to confirmed wrongdoing. This complicates presenting a unified donor front and weakens harmonisation efforts. It also affects incentives: agencies subject to strict repayment obligations may prioritise compliance and cost recovery more strongly, while in trust-based agreements the risk is effectively absorbed into the multilateral system.

Possible improvement

Closer alignment on repayment modalities would give donors stronger collective leverage and reduce fragmentation. A practical step would be to adopt a graduated system of obligations that several donors endorse. In this system, repayments would match the seriousness of the case: strict refunds in instances of fraud or corruption, joint consultation for losses from operational or administrative errors, and reprogramming as the default option where funds can be recovered without undermining programme delivery. This approach would bring predictability while still allowing flexibility in lower-risk cases.

Donors could also agree on joint procedures for recovery and reallocation in multi-donor initiatives. If rules are set in advance, agencies would not face a situation where one donor insists on repayment while others accept reprogramming. Harmonised modalities would also reduce transaction costs, since agencies would no longer need to follow different rules for each donor.

Transparency is another area for improvement. Even under UN rules, agencies should report systematically on the amounts recovered, repayment or reprogramming, and the reasons behind those choices. Clear reporting would reassure donors that risk-sharing does not mean opacity, and would encourage agencies to apply recovery measures consistently and fairly.

Taken together, these measures directly respond to the weaknesses identified in current framework agreements. Annex 1 provides a draft set of anti-corruption provisions that donors could use to harmonise language and streamline future agreements. These draft clauses are meant as a starting point for discussion and will need further development in consultation with donors and multilateral partners.

Addressing the gaps identified in this study will also require stronger cohesion among donors. The following section reviews existing coordination strengths and weaknesses before outlining possible ways forward.

Strengthening coordination between donor headquarters and permanent missions

Effective management of corruption risks in multilateral organisations depends not only on the strength of formal agreements but also coherent donor engagement across institutional levels. Headquarters set strategic priorities, but their effectiveness often hinges on how well they coordinate with permanent missions to multilateral bodies (for example in New York, Geneva, and Vienna) and with embassies in partner countries. When coordination functions smoothly, donors can combine strategic influence with operational oversight. As one Swedish representative explained, 'our ambassador meets regularly with the heads of UN agencies to stress the importance of risk management and transparency'.

In practice, fragmented responsibilities, weak information flows, and political constraints frequently undermine this coherence. The UNOPS scandal illustrates the risks: several donors remained unaware of serious irregularities until whistleblower disclosures reached the media. Without timely coordination between field-level observations and headquarters oversight, a unified donor response was delayed, allowing governance failures to persist unchecked.0181477ef055

This example highlights how structural and operational barriers limit donor capacity to prevent and respond to corruption risks. The following sections examine these coordination challenges in more detail, before turning to potential avenues for collective influence.

Fragmented structures and overstretched missions

Responsibilities for managing relations with multilateral organisations are often divided between different parts of donor governments. Headquarters usually lead on policy development, financial allocations, and the negotiation of framework agreements. Permanent missions represent donor interests at executive boards, provide intergovernmental oversight, and maintain broader diplomatic relationships. Embassies engage in programme-level monitoring and dialogue with partner governments. While this division of responsibility may be strategically logical, it can hinder anti-corruption oversight.

A visible consequence of this division is weak communication. Exchanges on integrity issues between headquarters and missions often lack formalisation, relying on ad hoc contacts rather than structured mechanisms. As one interviewee noted, 'the information flow is very variable, both sides are very busy, limiting donors’ ability to monitor and respond effectively'. Without clear channels for coordination, headquarters may underestimate the operational realities that missions face.

Capacity constraints add to the problem. A senior Finnish official explained, 'The MFA does not have enough resources to deal with all UN agencies and all the managerial implications it represents'. Governments often expect a single diplomat to represent their country across multiple UN executive boards in the same week, while also managing bilateral relations and core political priorities. As the Joint Inspection Unit has observed,1200e5ebd436 many Member State representatives serve on several governing bodies simultaneously, limiting the depth of oversight they can provide. As a result, technical oversight functions, such as monitoring anti-corruption safeguards, often receive less attention than politically visible concerns.

Political considerations further complicate the picture. Several interviewees observed that high-profile agencies such as UNDP, UNICEF, and WHO may receive less scrutiny due to their political and operational centrality. As one donor official put it, 'some agencies are just too important politically to confront directly'. Interviewees noted that political trade-offs often play a role. Maintaining influence on executive boards and preserving strategic alliances can take precedence over raising transparency concerns. As Thorvaldsdóttir7e7c912b898b observed, donors sometimes rely on informal channels rather than exerting pressure through formal mechanisms, particularly when reputational risks are at stake.

Missions also depend heavily on documentation from the agencies themselves. These reports are often incomplete, overloaded with irrelevant details, or written in bureaucratic language. This weakens donors’ ability to assess integrity risks in practice.6b96802aaae4 Such documents rarely capture on-the-ground realities, such as the quality of internal controls, the deterrent effect of whistleblower systems, or informal practices shaping fund management.

These constraints highlight the structural and political pressures shaping donor engagement. Overburdened staff, reliance on incomplete information, and political caution combine to reduce the consistency and quality of anti-corruption messaging at the multilateral level.

Building on these lessons, the following section outlines how a coordinated influence strategy can consolidate anti-corruption safeguards in multilateral partnerships.

Crafting an influence strategy to support multilateral oversight

The coordination challenges outlined above (fragmented responsibilities, weak information flows, overstretched missions, and political caution) limit donors’ ability to exercise consistent oversight of corruption risks. Recent experience shows that coordinated donor action can overcome these barriers.

Reforms on sexual exploitation and abuse (SEA) offer a clear precedent. Faced with reputational crisis and systemic safeguarding failures, donors developed a joint strategy that combined political pressure, harmonised standards, and technical collaboration. The following vignette presents the case and provides insights on priorities for donor engagement: building coalitions, harmonising framework agreements, broadening advocacy, and enhancing monitoring.

Good practice in donor engagement processes: SEA reporting

In 2018, Oxfam senior staff sexually exploited disaster survivors in Haiti, exposing systemic safeguarding failures.72fd45a5fc9b The scandal triggered global outrage, high-level resignations, and forced donors to act. They recognised the crisis as both a grave ethical breach and a reputational threat to the aid sector. The response showed that coordinated donor pressure, shared standards, and targeted mechanisms could produce institutional change across multilateral organisations.

At the core of this response was the establishment of a donor Technical Working Group (TWG), led by the United Kingdom and involving the United States, Canada, Germany, and France.8e241f69eac2 This group developed standardised SEA language and minimum requirements to be included in framework agreements. Donors also coordinated lobbying efforts to secure acceptance of safeguard clauses at the highest UN levels.

Reforms rested on three measures. First, framework agreements were harmonised to embed SEA provisions into core funding modalities. Second, reporting mechanisms were strengthened, such as the UNFPA iReport SEA Tracker. Third, donors demanded disaggregated data by gender, region, and type of allegation, improving risk analysis.

Coordination extended beyond the TWG through joint donor-multilateral platforms and independent expert groups. These bodies improved credibility and broadened advocacy beyond donor circles.

The reforms targeted culture as well as procedures. All UN staff are now required to complete mandatory learning on preventing SEA, and safeguarding is now systematically addressed in executive board discussions. Transparency challenges remain, as discrepancies persist between iReport and information presented to executive boards, but the principle is established: 'zero reports are now a red flag', as one FCDO officer explained.

Yet, as Westendorf and Dolan-Evans968530c5f433 observe, SEA functions remain fragile because they depend on earmarked funding and operate in silos, limiting institutional ownership.

The SEA precedent illustrates that collective donor action is feasible, even in politically sensitive areas. It also provides insight into how to address the structural and political pressures that undermine anti-corruption oversight.

The SEA case shows three key lessons: reforms were driven by donor coordination, not agency goodwill; cultural change mattered as much as technical fixes; and sustainability required embedding safeguards into core budgets and governance. These lessons are directly relevant to anti-corruption oversight, where fragmentation, weak reporting, and political caution continue to undermine donor influence.

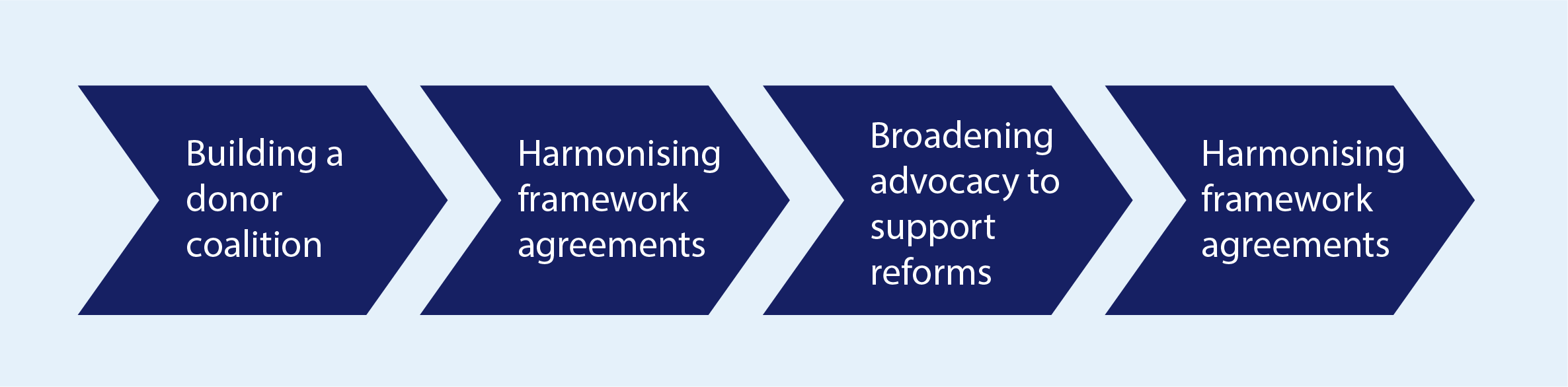

Similar to the SEA example, donors can pursue a phased influence strategy that aligns expectations, coordinates pressure, and tracks progress systematically. Figure 1 outlines this approach for strengthening anti-corruption safeguards in multilateral partnerships. It sets out concrete steps, beginning with coalition-building and moving through harmonised agreement clauses to systematic monitoring of key anti-corruption data. Taken together, these steps provide a pathway for shifting from fragmented oversight to coordinated engagement. The following section develops each step in turn.

Advocating for reform: steps for an influence strategy.

Source: developed by the author.

1. Building a donor coalition

Like-minded donors could form a coalition to define and promote common anti-corruption standards, modelled on the SEA Technical Working Group. The SEA case showed that collective action reduces political risk for individual donors. A coalition would also reduce fragmentation by linking headquarters officials and mission delegates in a shared forum, ensuring that political engagement and technical expertise reinforce each other.

By focusing on politically feasible areas, such as whistleblower protection or access to audit findings, donors could replicate the SEA experience. A practical first step would be to table the proposal at the OECD-DAC Anti-Corruption Task Team, which already convenes donor representatives and could anchor such a coalition.

2. Harmonising framework agreements

The SEA Technical Working Group successfully developed standardised safeguard language for framework agreements, easing the burden on agencies and closing gaps between donors. A similar approach on anti-corruption would reduce the inconsistency that weaken oversight. Harmonised anti-corruption provisions would increase safeguards but also reduce the workload of overstretched missions, which often struggle to track divergent donor requirements. Standardisation would also limit the reliance on ad hoc communication between headquarters and missions, giving diplomats a clear reference point when engaging with agencies.

Annex 1 presents a draft proposal for anti-corruption provisions that donors could use to harmonise language and streamline future agreements.

3. Broadening advocacy for agency reforms

The SEA response showed that reforms gained traction once advocacy extended beyond permanent missions to involve a wider set of actors, including civil society and technical experts. Broadening advocacy on anti-corruption can address political caution, distributing pressure across a wider coalition and reduces the reputational risks borne by individual donors.

Involving women’s organisations, oversight bodies, and anti-corruption commissions can also help ensure that issues such as gender-related vulnerabilities are not overlooked, while improving legitimacy and reducing the perception of donor-imposed standards. For instance, Gavi's Independent Review Committee incorporates technical experts from various countries to assess funding applications, promoting transparency and accountability. These models show that shared ownership can increase credibility and build more durable coalitions for oversight.

4. Enhancing anti-corruption monitoring

The SEA experience showed that sustainability requires robust monitoring systems embedded in institutional routines. Mechanisms like the iReport system and the use of disaggregated data demonstrated how transparency improves if monitoring is systematic and independent.

For anti-corruption, the independent Multilateral Organisation Performance Assessment Network (MOPAN) could play this role by conducting regular reviews of safeguards such as whistleblowing channels and access to audit findings. This would provide evidence that overstretched missions cannot easily collect themselves and would offset the reliance on incomplete or overly bureaucratic agency reports.

For monitoring to be effective, it must be politically supported, resourced, and insulated from selective reporting, all weaknesses that undermined donor oversight in the UNOPS scandal.

Conclusion: from fragmented oversight to collective influence

Framework agreements remain donors’ primary contractual tool for shaping integrity standards in multilateral organisations. They matter because they establish baseline expectations on reporting, investigations, and audit access.

Yet this review shows that many of these provisions are either weakly formulated, inconsistently applied, or missing altogether. In particular, fraud reporting obligations defer to agencies’ discretion, audit access is inconsistently granted, evaluation rights are limited, and verification through site visits is rare.

Improvements are possible through clearer requirements and stronger enforcement clauses. Donors could press for systematic and timely fraud notification, consistent access to audit findings, clearer provisions for independent evaluations, stronger protection for whistleblowers, and rights to verify through site access. Examples such as Finland’s site visit clause demonstrate that these safeguards are politically and legally feasible.

Still, framework agreements alone cannot ensure effective oversight. They provide a necessary baseline, but their reach is limited: they do not replace organisational reforms, governance changes at board level, or sustained donor follow-up in the field. Fragmented donor structures, overstretched missions, and political trade-offs further limit the enforcement of technical safeguards. The SEA precedent nonetheless shows that collective donor action, when reinforced by political pressure and systematic monitoring, can overcome these limits.

Accordingly, the way forward lies in combining improved anti-corruption provisions with a phased influence strategy: building coalitions, harmonising language, broadening advocacy, and reinforcing monitoring. Framework agreements can narrow critical gaps and provide a common standard, but only coordinated donor engagement can turn them into effective safeguards.

Annex 1

Anti-corruption requirements in framework agreements

The following model provisions reflect the weaknesses identified in current donor agreements. They are structured according to six core areas of access and oversight, with cross-cutting safeguards on whistleblowing and gender responsiveness. They are intended as a menu of clauses to support greater harmonisation across future agreements.

1. Financial information

1.1. Risk-related financial information

Model clause

The partner must provide the donor with annual financial statements accompanied by risk-related financial information. This should highlight vulnerabilities in partner selection, fiduciary safeguards, and budgetary controls, and describe corrective measures undertaken.

Rationale

Dedicated reporting on risk-related financial information provides a structured overview of systemic vulnerabilities and the adequacy of mitigation measures. By presenting this information in a consolidated format, donors can assess fiduciary risks more effectively and prioritise their oversight efforts. Such reporting can be negotiated without undermining the single audit principle.

1.2 Granularity of financial information

Model clause

The partner must provide the donor with certified annual financial statements that link expenditures to budget lines and results, and disaggregate contributions by sub-programme, activity line, and when relevant earmarked funding. Reports must include explanations of significant variances.

Rationale

Granular financial information makes it possible to trace how contributions are used, connect spending to intended results, and detect inconsistencies or unusual patterns. This level of detail is essential to strengthen accountability, assess value for money, and support early identification of irregularities.

1.3 Implementing partner disclosure

Model clause

The partner must disclose to the donor the list of implementing partners engaged under the donor’s contribution, and confirm that none are subject to sanctions lists.

Rationale

Implementing partners often manage significant portions of funds, yet can be a major source of fiduciary and reputational risk. Disclosure obligations enable donors to verify eligibility, confirm compliance with sanctions regimes, and ensure that contributions are not channelled to high-risk or prohibited entities.

1.4 Usability of oversight information

Model clause

The partner must structure audit and financial material in a way that enables the donor to identify priority risks. Reports should highlight key findings, systemic issues, and corrective actions.

Rationale

Oversight is effective only if the information provided is accessible and actionable. Structured and prioritised reporting enables donor staff to focus on the most critical risks, strengthens early warning capacity, and enhances the collective accountability of multilateral partners.

2. Fraud reporting

Model clause

The partner must notify the donor without undue delay of any credible allegation or confirmed instance of fraud, corruption, or other financial misconduct relating to activities financed by the donor. Notification must take place where substantial fiduciary or reputational risks are present, including at the stage of suspicion, and must not be limited to cases where allegations are fully substantiated or investigations are concluded.

Notifications must comply with applicable legal agreements, the United Nations single audit principle, and safeguards relating to confidentiality, whistleblower protection, and due process. Each notification must, at a minimum, specify the nature of the allegation, the programme or office concerned, the status of internal review, and any interim measures adopted. In the context of multi-donor initiatives, the partner must apply harmonised notification protocols agreed with all donors to avoid duplicative demands on investigative capacity.

Notifications must, where applicable, include gender-disaggregated data and analysis of risks disproportionately affecting women and marginalised groups.

Rationale

Current practice allows agencies wide discretion in the timing and content of fraud notifications, often resulting in significant delays. A contractual obligation for early, standardised, and risk-sensitive notification would enable donors to protect funds, coordinate responses, and strengthen collective oversight, while still respecting the safeguards required under international agreements.

3. Evaluation rights

Model clause

The donor must have structured opportunities to contribute to the design, scope, timing, and methodology of evaluations of donor-funded activities. The partner must ensure that such opportunities are systematic and not limited to ad hoc arrangements.

Subject to the partner’s approval, the donor may lead an evaluation, in particular for projects of significant financial value or operating in high-risk contexts. In such cases, the partner must facilitate access to information and cooperation necessary to carry out the evaluation.

The partner must also commission independent third-party evaluations for projects exceeding a defined financial threshold or operating in high-risk contexts.

Evaluation findings must be disclosed publicly, except where security or legal concerns provide a justified limitation.

Rationale

Most agreements restrict evaluation rights to agency-led processes, leaving donors dependent on outputs controlled by the partner. Precedents from Finland and Norway show that, with approval, donors may occasionally lead evaluations. Germany demonstrates that donors can influence scope and methodology even when evaluations remain partner-led. A contractual provision recognising these options would give donors stronger and more predictable participation while respecting the partner’s governance framework.

4. Site access

Model clause

The donor shall have the right to conduct site visits or field verifications of donor-funded activities as a complement to desk-based oversight. Such visits must be coordinated with the partner to avoid disruption and shall respect the partner’s internal regulations and procedures. For consistency and accountability, these rights must apply across all donor-funded activities, not only when the donor participates in UN-led evaluation missions.

Rationale

Only Finland and Switzerland currently grant explicit rights. Wider adoption would support direct verification of implementation and strengthen incentives for country-level integrity.

5. Repayment modalities

Model clause

The partner must apply a graduated system of repayment obligations, calibrated to the seriousness of the case. In cases of fraud or corruption, strict repayment to the donor is required. In cases of operational losses or administrative errors, repayment must be determined through joint consultation between the partner and the donor. In lower-risk cases where programme delivery can be safeguarded, the default must be reprogramming of recovered funds. For multi-donor initiatives, the partner must apply harmonised procedures agreed ex ante by all participating donors. The partner must also provide systematic disclosure of amounts recovered, the decisions taken on repayment versus reprogramming, and the rationale for those decisions.

Rationale

A harmonised, graduated repayment regime upholds zero tolerance for fraud, while allowing flexibility for reprogramming of funds in lower-risk cases. It would safeguard delivery, protect beneficiaries (including women and marginalised groups), and improve accountability through systematic disclosure.

6. Cross-cutting safeguards

a) Whistleblowing

The partner must maintain accessible, confidential, and gender-sensitive reporting channels aligned with ISO 37002:2021. Whistleblowers shall be protected from retaliation. Staff perception surveys must be conducted periodically to monitor trust in reporting mechanisms and leadership commitment to integrity.

b) Gender-responsive anti-corruption

The partner must integrate gender-responsive approaches into risk assessments, including the monitoring of SEA and sexual corruption, gender-disaggregated reporting of misconduct, and targeted safeguards to protect women and marginalised groups.

Rationale

Whistleblower protection and gender-sensitive approaches are essential to move beyond procedural safeguards and ensure that integrity measures are inclusive and effective.

- OECD 2025

- Runde and Hardman 2024.

- OECD 2024.

- JIU 2023.

- Canada (Global Affairs), Denmark (Danida), Finland (Ministry for Foreign Affairs), Germany (BMZ and GIZ), Norway (Norad), Sweden (Sida), Switzerland (SDC), United Kingdom (FCDO).

- Trithart and Romier 2025.

- Vinjamuri 2025.

- CEB Audit and Inspection 2005.

- See Ainsworth 2022.

- Nicaise and Franchini 2025.

- JIU 2023b.

- 2016.

- Nicaise and Franchini 2025.

- Relief Web 2019.

- ICAI 2021.

- 2024.