1. Resource extraction and multilateral governance of the seabed

This U4 Issue examines potential conflict of interest and corruption risks within the International Seabed Authority (ISA) and proposes reforms to address some of these gaps. By identifying vulnerabilities in current procedures and institutional design, the analysis aims to strengthen the ISA’s legitimacy and ensure that seabed resource management aligns with principles of transparency, accountability, and global equity. The ISA is an intergovernmental organisation established by the 1982 United Nations Convention on the Law of the Sea (UNCLOS).be1b872271b9 Headquartered in Jamaica, the ISA governs the minerals in the international seabed beyond national jurisdiction making up roughly half of the Earth’s surface known as ‘the Area’.8ff9f3638d30

The organisation’s core mandate is twofold: to regulate exploration and exploitation of the Area’s minerals for the benefit of all of humankind, and to ensure effective protection of the marine environment from the harmful impacts of such activities.52363f55916c The ISA, via its parties (170 member states plus the European Union) promotes scientific research, develops policy and legal frameworks, issues exploration contracts, and is currently negotiating a mining code to regulate future mineral exploitation operations.346f3c83ee62

Rising global attention on deep seabed mining

Deep seabed minerals were first discovered in the nineteenth century, and their commercial exploitation has been talked about since the 1960s. But mining at the depths required (<6000m) has never been pursued at commercial scale due to regulatory uncertainty, technological and economic barriers, and more recently also by environmental risks.

Global attention on deep seabed mining has lately intensified as the demand for alternative sources of ‘critical minerals’ grow. Metals like cobalt, copper and nickel, sought after for the energy transition, digital infrastructure, and defence technologies, are contained in deep seabed mineral deposits, These divide into different types with different features called: polymetallic nodules, cobalt-rich crusts, and seafloor massive sulphides.fc8e981b26d2 Where located in the Area, those minerals are designated ‘the common heritage of humankind’.b18dca9abfd9 Burgeoning interest is met with mounting concerns entwining environmental, economic, social, and governance risks. A particular focus is the data limitations to inform decisions that may irreversibly harm fragile and little-understood deep-sea ecosystems.887ce3e97726

Fractured multilateralism of ocean governance

As of 2025, 20 countries are sponsoring ISA contracts to explore the Area as a precursor to deep seabed mining. Meanwhile, 40 countries have called for a moratorium or precautionary pause on deep seabed mining until more robust scientific assessments and environmental safeguards are in place.d9ee69e1fd4f

Tensions on deep seabed mining regulations heightened further in April 2025 when the United States, which is not a party to UNCLOS, moved to bypass the ISA altogether. Using a US domestic law that pre-dates UNCLOS, the White House issued an executive order to expedite unilateral seabed mineral licensing in the Area.ab4c86e3bb5f A Canadian firm The Metals Company, through a US subsidiary, applied to the US government for exploration and commercial recovery permits over these minerals despite UNCLOS’ prohibition over their exploitation outside of the ISA’s regime.db2f7580cb7f Such developments risk undermining the ISA’s authority, the principle of the Area as the common heritage of humankind, and the global order of ocean governance.

Reinforcing the foundations of seabed governance

In this context, the ISA is under increased scrutiny of its fitness-for-purpose as a regulator of the global commons. Structural and governance vulnerabilities at the ISA have received recent critiques in both academic literature and the ISA’s own deliberations.5a125500f526 In recent years a number of serious allegations have also been made publicly in the media, including in high-profile features by global media outlets (including the LA Times, The Guardian, Bloomberg, and New York Times).940ff7ada5e4 The claims made in these pieces concern among other things: misuse of funds, inadequate financial controls, bribery of public officials, opacity, corporate capture, undue influence by certain factions over ISA governance, and inappropriate favouring of private economic interests.1854ab5adda8 The ISA Secretariat issued a press release presenting their own version and denying misconduct.1e75bff0dfad There does not appear to have been any attempt, nor is there an available mechanism, for independent investigation of these allegations.

In the short-term, evidence of the ISA’s structural and administrative vulnerabilities erodes legitimacy and trust. This comes at a time when the ISA needs credibility to withstand the threat of US unilateral action and when the ISA is examined as a precedent for new Biodiversity Beyond National Jurisdiction (BBNJ) governance arrangements that came into force in January 2026. If the ISA loses support from primary members and stakeholders, it could more widely trigger fragmentation of global governance, undermine multilateralism, and corrode the very idea that shared resources can be governed fairly and sustainably.

This U4 Issue provides an evidence-based analysis of corruption and conflict of interest risks within the governance structures of the ISA. This analysis avoids assessing specific corruption claims that have been levied at the ISA but seeks instead to highlight institutional vulnerabilities that could be improved upon to better serve the ISA’s mandate. It outlines strategic recommendations for strengthening safeguards to ensure ISA decision-making is transparent and accountable in line with its foundational principles of equity, environmental stewardship, resource development, and the common heritage of humankind. The first section provides a light touch review of conflict of interest and corruption risks within the extractive sector as they pertain to the ISA. The U4 Issue moves on to provide an analysis of potential conflict of interest risks that emerge from, first, the ISA’s legal and institutional structure outlined in UNCLOS and, second, the ISA’s administrative and procedural processes.

Conflict of interest in the context of international resource governance: Relevance to seabed mining

The ISA is arguably at particular risk of potential conflicts of interest due to the correlations between nature resource endowment and corruption. Conflict of interest risks in extractive industries are amplified by drivers of corruption (meaning a force that motivates individuals to engage in corrupt practices), and enablers of corruption (meaning the institutional weaknesses that make corruption easier to commit and harder to detect) (see table 1).0faab13cb02e

Table 1: Enablers and drivers and corruption in the natural resources sector

|

Drivers |

|

|

Enablers |

|

Risk of political and regulatory capture by private interests is exacerbated where there are opaque processes, lack of oversight, and gaps in enforcement.7d7360bc04bb This can manifest through bribery in licensing and contract awards or regulatory evasion and environmental non-compliance. The effects of corruption in extractive industries may include environmental disaster, marginalisation and abuse of affected communities, loss of public revenue, and loss of public trust in the government. A parallel to the perils in early phase of deep seabed mining, including power and technological asymmetries, gaps in governance, and ecological risks, can be drawn with the experience of early resource extraction in Nigeria or Angola, where corporations entered with capital and technical knowledge, paid bribes to elites to facilitate extraction, and left with the profits.77a899d4f5e7

Box 1: Definitions in this U4 Issue

Conflict of interest

– a situation where public officials’ private interests could improperly influence the performance of their duties, including actual, potential, or apparent conflicts.

Regulatory capture

– occurs when regulatory agencies become dominated by the industries they regulate, leading them to act in the interest of those industries rather than the public.

Cronyism

– a form of corruption where friends, associates, or insiders are given preferential treatment, including appointments or advantages not based on merit.

Undue influence

– the act of exerting improper pressure or manipulation that overcomes another person’s free will, leading them to act against their independent judgement.

Beneficial ownership transparency

– the disclosure of the real, natural persons who ultimately own or control a legal entity.

While corruption risks in extractive industries are broad and systemic, conflicts of interest represent a particularly acute vulnerability because decision-makers often hold overlapping roles or financial stakes that can compromise impartial governance. The OECD defines conflict of interest as ‘a conflict between the public duty and private interests of a public official, in which the official’s private interests could improperly influence the performance of their duties’.5fc2484bdece Such conflicts can be actual, potential, or apparent.c02995c4924d Moreover, conflicts of interest can be of an indirect nature, meaning they could pertain to any advantage (or liability) not only to (or for) the public official but also to their family, close relatives, friends, and persons or organisations with whom he or she has or has had business or political relations.52bfd691796f The UN Convention against Corruption (UNCAC), of which all but two ISA member states are signatories, requires each state party to adopt systems to prevent conflicts of interest.166165721a49 The implementation review mechanism under UNCAC touches on extractive industries, but the peer review mechanism overlooks international bodies such as the ISA.

Whilst deep seabed mining faces similar potential conflict of interest risks to those observed in existing extractive industries, there are also peculiarities specific to the ISA that can heighten those risks. In the ISA’s case, the rules for mining are not yet settled. Some commentators frame deep seabed mining as a ‘high-risk, high return’ investment, whilst others question that it is commercially viable at all.3880ef7beb05 Commercial viability of deep seabed mining in the Area will depend specifically on how the ISA sets its financial, benefit-sharing, operational, and environmental rules – the parameters of which are still under negotiation.5e7f4fce887a This means that there are major incentives at this time for potential extractive industry actors to seek to influence the regime in their favour. Any attempt to regulate capture should ‘explicitly integrate an assumption that corrupt actors will push back against particular reforms or enforcement actions’.fffab3bbd6f6

2. Vulnerabilities at the ISA

The ISA’s legitimacy rests on its mandate to act as a neutral steward of the Area and to represent the interests of humankind as a whole.b2ffa7c636d3 If the ISA were compromised by corruption and undue private influence the consequences would be profound. On several occasions, public sources including the mainstream media has called into question the integrity of the ISA. The following analysis, which draws upon a body of academic research,6bb8d800dd43 highlights particular features of the ISA that expose the institution to particular risk of undue influence caused by conflict of interest or corruption.

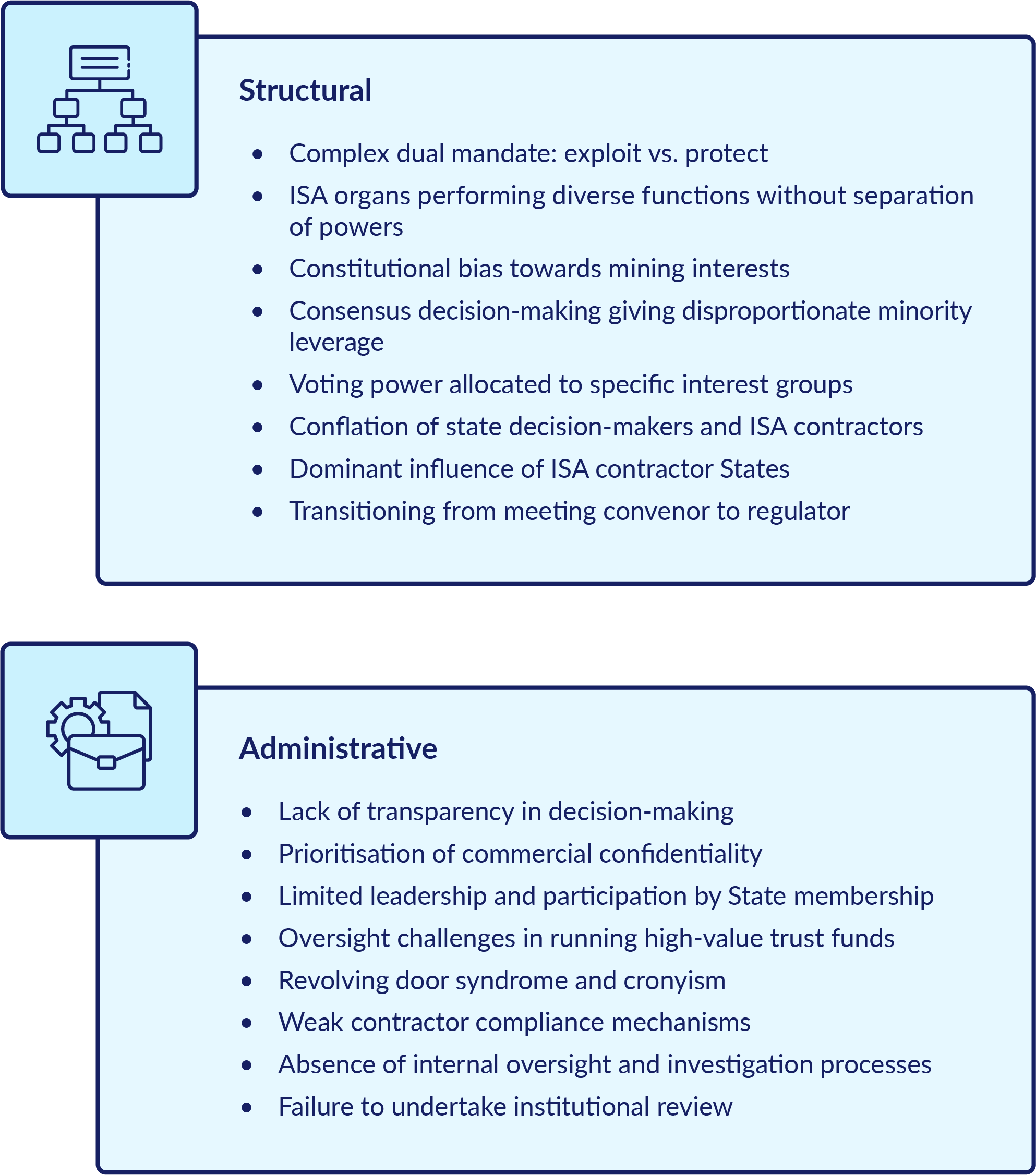

These are divided into two categories: structural challenges and administrative measures – as summarised in Figure 3.

The structural category (section 2.1) recognises that the ISA’s institutional structure and high-level governance arrangements are dictated by the provisions of UNCLOS and are in many respects outside the immediate control of ISA actors. Anti-corruption reform in relation to these features may therefore need to focus on mitigation and management of those risks, rather than the root causes.

The administrative category (section 2.2) relates to institutional processes and policies that would be within the ISA’s power to develop and implement and can help manage risks presented by the structural vulnerabilities.

If not addressed, the individual features identified in section 2.1 (structural) and section 2.2 (administrative) combine with each other, further compounding risk.

Figure 3: ISA vulnerabilities to conflict of interest

2.1 Structural factors heightening potential conflicts of interest in the ISA

A complex dual mandate: to exploit vs. to protect

All the ISA organs have a complex dual mandate: to facilitate mining on the deep seabed, whilst also protecting the marine environment. The juxtaposition of extractive and conservation objectives creates a structural conflict.2141e1c4b9fe This is compounded by the obligation of the ISA (and its member states) to act as representatives of the interests of humankind, invoking a wider set of ‘public’ interests and concerns. Difficulties in reconciling these competing mandates may expose the ISA to interest lobbying and incentivises regulatory capture.

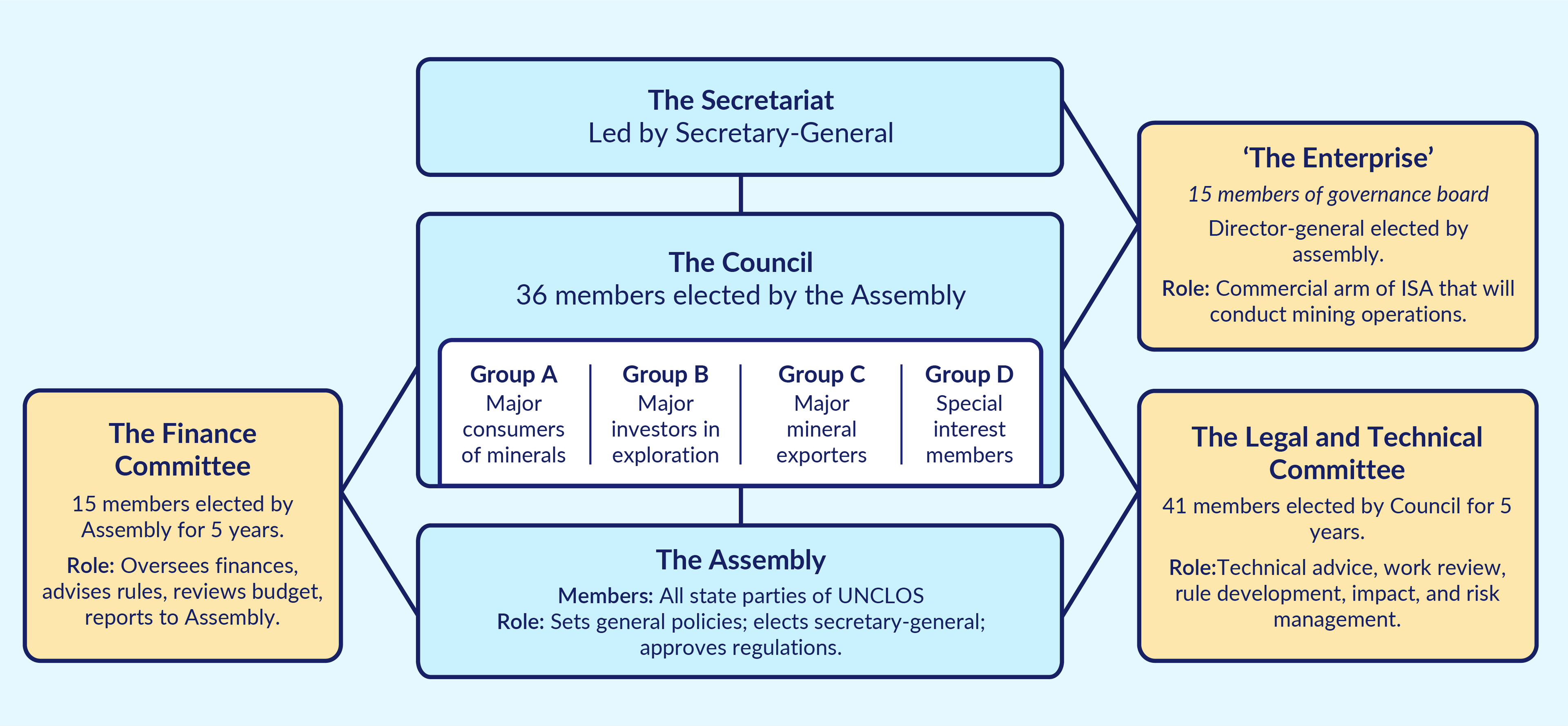

Figure 4: Organisational chart of the ISA

Credit: ISA 2025f, p. 110.

The organs of the International Seabed Authority performing diverse functions without separation of powers

The same ISA organs (and often the same individuals) are responsible for the ISA’s core functions: rulemaking, contract award, regulatory enforcement, and financial oversight (see Figure 4). The ISA may also in the future both regulate and operate its own in-house mining arm (‘The Enterprise’) that will initially function via joint ventures with private interests. When a single authority is responsible for writing, applying, and enforcing the rules, this can undermine checks and balances, reduce impartial scrutiny, and enable self-serving interpretations. At present, the ISA’s advisory and decision-making bodies do not appear to have mechanisms in place to ring-fence such potentially conflicting functions. This exposes the ISA to risk of capture by specific interest groups.027473dcef47

Constitutional bias towards mining interests

UNCLOS Part XI was drafted with an assumption that deep seabed mining will occur, with exploitation as the foundational purpose to the ISA’s existence.bfee29935f18 Although any such mining would need to be undertaken within parameters that protect the marine environment – a duty the ISA takes seriously – if mining does not proceed, the rationale for the ISA’s relevance and scope may be weakened. Furthermore, the ISA is intended to become self-funded from mining revenues. Without mining, the ISA is dependent on voluntary contributions from states. The organisation’s budget and relevance depending upon mining exploitation can incentivise a bias toward commercial interests at the cost of science-based and impartial decision-making pursuant to legal requirements such as the precautionary approach and the broader interests of all of humankind. Member states have financial incentive to accelerate or facilitate award of mining contracts to end the financial contributions they have been paying to the ISA for 30 years.39a48e07b946

Consensus basis giving disproportionate minority leverage

UNCLOS (and its Part XI Implementation Agreement) require the ISA to operate as a consensus-based regime.d3523368bb9f This means all parties work to adopt decisions without formal voting. For some but not all ISA decisions, voting can take place if consensus cannot be reached. In practice, the ISA has never held a vote on any regulatory, legal, policy, or contractual matter.e4440e20222b Voting has only occurred to date in the context of Secretary-General elections. A consensus-based decision-making model can inadvertently heighten the risk of corruption and institutional capture. When a small bloc or even single state can veto decisions supported by a broad majority, it creates disproportionate leverage, allowing actors with vested interests to block reforms, dilute standards, or extract concessions. This dynamic at the ISA is also vulnerable to potential conflicts of interest if the blocking state has vested interest in the decision in question eg as an ISA contract-holder or as a country with particular opposition to deep seabed mining.e68bb4871313

Voting power allocated to specific interest groups

The ISA’s executive body, the Council, comprises 36 countries allocated into a series of chambers (see Figure 4). Each chamber must have a majority for certain votes to pass. These chambers include: four countries with the highest consumption or imports of relevant metals; and four countries who are the largest investors in deep seabed mining in the Area. To disapprove award of a mining contract requires a super-majority (two-thirds) of council members, and a majority in every chamber. It is therefore expressly devised in the ISA’s voting structure that specific interest groups exercise weighty influence on crucial decisions. Due to the small size of some of the voting chambers (four countries), and possible absences or abstentions, just one or two countries could have the power to decide final outcomes.a8e4f57a5179 This entrenches a governance model whereby outcomes can be shaped by those with the most to gain financially or strategically. Voting structures that reward strategic alliances, or economic sponsorship may incentivise behind-the-scenes deals, vote trading, or political bargaining.

Conflation of state decision-makers and ISA contractors

All ISA contracts must be held by, or sponsored by, an ISA member state. The ISA system requires states collectively to contract with and regulate states individually. Most current ISA contracts are held directly by 100% state-owned entities. The contractor or its sponsoring state is usually also a member of the ISA organs that regulate its own activities. State and contractor interests may be conflated. In addition, respect of sovereign rights, diplomatic protocol, fear of retaliation, power asymmetry, and trade relations can affect states’ willingness to regulate another state. This is typical for negotiations in the United Nations and other international organisations, but it is not typical to simultaneously hold contractual and regulatory relationships with individual state members as the ISA does.

Dominant influence of contractor states

Frequently, the same nations, and in some instances, individuals, are represented across each organ of the ISA. Some examples never queried during ISA proceedings include:

- In 2025, nine countries were at the same time represented on all of the ISA’s advisory and decision-making bodies ie the Assembly, Council, Legal and Technical Commission (LTC), and Finance Committee, whilst also holding or sponsoring ISA contracts that these organs are regulating.db8086cc010c

- In 2022, the President of the Council was also the head officer of an ISA exploration contractor.33400da6e0be

- In 2020, the same country presided over all three of the ISA’s most influential organs (the Assembly, Council, and LTC) at the same time, and in the same session that this country sponsored an application for an ISA contract.c50869e70f62

If the same states and individuals can simultaneously shape, implement, and benefit from ISA decisions, this creates systemic risks for conflicts of interest. A state cannot unilaterally decide what happens with a contract, nonetheless, with representation in every ISA organ can disproportionately influence decisions for the benefit of a few, rather than for the good of humankind. Overrepresentation could also allow a small number of states with specific interests to dominate agenda-setting, shape regulatory outcomes, and suppress dissenting views. When the same actors populate all main bodies, it weakens internal accountability and oversight and blurs the separation of functions. Although the LTC was set up by UNCLOS to be a technical advisory body, voting structure that makes it difficult for the Council to go against an LTC recommendation (eg for an award of a contract) gives LTC members significant influence over important decisions. Appointment of LTC officials also working for sponsoring states or contractor entities may potentially blur the separation between regulatory judgement and the commercial interests of member states.

Transitioning from meeting convenor to mining regulator

At this juncture in 2025–2026, the ISA is transitioning from its past role as a UN-style meeting convenor focused on learning, norm-setting, and light-touch exploration oversight towards becoming an active regulator of deep seabed mining. This shift demands a fundamental upgrade in institutional capacity, transparency, and accountability mechanisms to match its evolving regulatory authority. Admittedly, this period will take time. It may be years yet until the Regulations are adopted and an application is received and approved, and more years still until any mining actually takes place. Hence, the ISA must take an evolutionary approach to becoming a regulator. During this period, risks of potential conflicts of interest may escalate as the ISA’s responsibilities grow and complexify. The potential consequences of opaque procedures, confused mandates, personnel overlap, etc., are only likely to intensify when there are strategic mineral rights, potential serious environmental harm, and large sums of revenue involved.

2.2 Administrative and procedural factors heightening potential conflicts of interest in the ISA

Below, we set out administrative decisions or mechanisms within the control of ISA actors, which may contribute to the portfolio of potential conflict of interest risks faced by the ISA.

Lack of transparency in decision-making

Whilst decisions of ISA organs are published, these generally do not set out the reasons for the decision. Although ISA sessions are livestreamed – which is a very helpful practice – neither the audio and video recordings nor any full written record of the ISA’s deliberations are made available. The LTC and the Finance Committee meet in private and provide only very brief reports. While private LTC deliberations may shield members from direct political pressure, this protection does not preclude the need for stronger, carefully designed transparency measures that enhance accountability without exposing individuals to undue influence. ISA contracts are not published. There is no published beneficial ownership registry, or registry of disclosure of interests.

Ongoing scrutiny of behaviour provides a strong deterrent against conflicts of interest, but piecemeal information is insufficient.c1d782d9ca05 A regime defaulting to secrecy can allow individuals or groups to hide conflicts of interest and to pursue private interests without oversight. This increases risks of unethical behaviour, biased or flawed decisions, and corrupt practice (eg self-dealing, kickbacks, favouritism).

Prioritisation of commercial confidentiality

Protecting commercial sensitivity is given outsized regard. A broad definition of ‘confidential’ has been applied at the ISA encompassing ISA contracts, plans of work, contractor annual reports and data. Non-disclosure agreements are used by the secretariat eg for science expert working groups. In many cases information about contractor performance is not even disclosed to the ISA’s executive body, the Council, who are ultimately responsible for supervision of their activities.408f6df100ab

The lack of visibility around ISA contracts and contractor data could enable contractors to cut corners, misreport, or engage in corrupt practices with little risk of exposure. The closed nature of LTC meetings also prevents two-way information flows between the LTC and the ISA’s various stakeholders that could enhance knowledge to support more inclusive and informed decision-making.

Limited leadership and participation by states

The ISA experiences limited engagement from its state membership. The majority of states are in arrears with their assessed contributions to the ISA’s budget, and the Assembly rarely achieves its 50% quorum. In this context, subsidiary and technical organs of the ISA tend to shoulder significant workload (LTC, Finance Committee, Secretariat), but there is an absence of clear allocation and express delegation of responsibilities to these organs from the executive and political state-led bodies (Council, Assembly). Ambiguity in respective organs’ roles, accountabilities and powers weakens internal oversight and allows burden-shifting whereby subsidiary bodies operate with excessive autonomy and power.252ced62d774 This can lead to capture and overreach of authority with policy being set from the bottom up by a small number of individuals, without transparency or accountability to the wider membership. Lack of scrutiny and instruction from the political bodies heightens potential risk of conflict of interest by creating opportunity for undue influence over decision-making.

Oversight challenges in running high-value trust funds

The ISA plans to manage in-house a series of funds for:

- Common heritage – pooling royalty revenue.d1613bb111c2

- Partnerships – science and capacity-building grants.d24fcba9d2a1

- Environmental compensation – to help cover liabilities that may be caused by ISA mining.7656cf8e0493

- Economic assistance – to compensate land-based mining countries whose economies are seriously affected by deep seabed mining.97df96cbca38

Eventually, these could together hold vast sums of money. The ISA is a small intergovernmental body with 37 staff members and limited financial oversight infrastructure. It is required to take an ‘evolutionary approach’ to the setting up and the functioning of its organs and subsidiary bodies.0febf5b9d395 Managing multiple high-value funds demands robust accounting, auditing, and fiduciary controls in excess of ISA’s current capacity. Unlike other global fund-holders, the ISA lacks an independent board or fiduciary trustee.fc64282c30e3 These gaps, combined with opaque governance structures, may leave fund management vulnerable to misallocation, favouritism, or misuse. If the same actors who regulate mining or who directly benefit from fund disbursement, are responsible for disbursement decisions, it may create a potential conflict of interest.

Revolving door syndrome and cronyism

The expert pool for deep seabed mining is small and often geographically skewed, due in part to the high costs and technological challenges of studying relevant sites. Procurement of experts by the ISA for working groups, workshops, and consultancies has been managed in an ad hoc and sometimes opaque manner.2e9bb970af92 Decisions on staffing have been questioned (by the Finance Committee, the Assembly, and by disgruntled staff members via tribunal services). Whilst members of the LTC are required by UNCLOS to ‘have no financial interest in any activity relating to exploration and exploitation in the Area’,82245dc91d36 LTC members have been identified as employees of ISA contractors, with no apparent repercussion.1a1796c2c886 The ISA is subject to ‘revolving door’ syndrome, where individuals shift between secretariat, political, advisory, and contractor roles. Such personnel may face divided loyalties. The ISA’s integrity can be undermined if individuals are perceived to be able to shape policy decisions to benefit factional interests. Persons moving from the ISA to the industry may exploit privileged knowledge of internal processes, networks, or decision-makers. This creates an uneven playing field, disadvantaging other stakeholders and undermining procedural fairness. Where procurement and recruitment processes are opaque, and conflict of interest measures are not enforced, revolving door and cronyism risks are amplified.

Weak contractor compliance mechanisms

The ISA faces significant challenges with managing an industry that takes place thousands of miles from shore and far below sea-level. To date it exhibits systemic weaknesses in compliance oversight and enforcement of its rules on two levels. First, there does not appear to be an internal compliance function designated within the Secretariat to monitor and enforce institutional rules.d3c406fc7c0b Second, contractor regulation relies almost solely upon self-reporting. Plans for a staff of inspectors, and a compliance committee remain under discussion. Where non-compliance (either by contractors or by ISA insiders) has been flagged, administrative or regulatory response by the ISA has been slow, uncertain or absent.e5de1c4b2223 This is relevant because actors with vested commercial or political interests can operate with minimal scrutiny in an institutional and regulatory system that does not proactively monitor and enforce compliance. This may enable selective reporting, regulatory leniency, and undue influence over decision-making processes. The lack of robust independent verification, clear regulatory response pathways, and public accountability, all contribute to a climate of impunity.

Absence of internal oversight and investigation processes

The ISA is an autonomous international organisation and not an agency of the UN and so does not fall under the purview of the UN’s Office of Internal Oversight Services, Independent Audit Advisory Committee, Board of Auditors, Joint Inspection Unit, or Ethics Office. The ISA has not established its own version of these mechanisms. It has no Ombudsperson, nor even basic recourse for public complaints. Despite operating as a regulator of hi-tech, complex, and remote operations, there is no whistle-blowing procedure in place.9f460319af76 The principal oversight mechanisms are the (largely ceremonial) one-week annual session of the ISA’s Assembly, and on financial matters, an annual three-day meeting of the Finance Committee. In practice, the ISA appears to operate day-to-day without independent scrutiny of its financial management, personnel conduct, or regulatory decisions. This could allow abuse of authority, misconduct, conflict of interest, undue influence, or poor decision-making to go undetected and without repercussion.

Failure to undertake institutional review

The Assembly is mandated to undertake a general and systematic review every five years of the way the ISA’s regime has operated.52d32f6a5ba8 These provisions have been largely overlooked during the ISA’s tenure. Only one of the periodic reviews has taken place in the institution’s 30-year operating history. Uptake of the recommendations from that review (dated 2016–2017) remains piecemeal. A permissive situation for corruption and mismanagement is created if the ISA consistently fails to implement its mandated oversight and review duties. Absence of institutional accountability mechanisms at the ISA can enable entrenched interests to operate without challenge, weakening the checks and balances necessary to manage conflicts of interests and to prevent abuse of power and regulatory capture.

3. Opportunities for reform

Timing

The ISA is perfectly placed to address these issues now. The institution and the sector are preparing to move from deep seabed exploration to exploitation for the first time, which means measures can be established now before the risk profile escalates. Establishing the institutional framework before allocation of mining rights supports stronger governance.29b22d763e70 The ISA is negotiating its Exploitation Regulations now, which presents a timely opportunity for legislative embedding of accountability measures. This is strengthened by the tenure of a new Secretary-General started in post in 2025, after eight years of the previous administration, and has made various public commitments towards reform and accountability.2231e6f7fd7c

The overdue periodic review into the ISA’s functioning, required under Article 154 of UNCLOS, is likely to kick-start in July 2026, and a new multi-year Strategic Plan is also due for development in the same timeframe.

Drawing on international standards

The ISA is a unique institution in some ways but nonetheless can learn from a wealth of existing precedent and learned experience.3832bb5551f1 Systems for good governance in public institutions, and measures to address corruption in extractive industries, are not new. The ISA could benchmark itself against and draw from various existing standards at the international level. The Aarhus Convention (1998) and the Escazu Agreement (2018) provide useful pillars for access to information, public participation, and access to justice. There is a wealth of relevant non-binding guidance eg OECD’s Ministerial Recommendation on Transparency and Integrity in lobbying and Influence (2024), and the World Bank, OECD and UNODC’s Toolkit on ‘Managing conflict of Interest in the public sector’ (2020), UNDP anti-corruption frameworks, and the systems employed by multi-stakeholder initiatives such as the Extractive Industries Transparency Initiative, and the International Aid Transparency Initiative. Non-governmental sources include guidance from Transparency International, and the Natural Resources Charter and its Benchmarking Framework (2015), and standards from the International Organisation for Standardisation (such as ISO 37001: 2025 on an Anti-Bribery Management System).

Drawing on the United Nations

The ISA is not part of the UN, but UNCLOS does require the ISA Council to ‘enter into agreements with the United Nations or other international organizations’.3f2cc2762edc In 1997, the two Secretary-Generals of the ISA and the UN respectively signed a Relationship Agreement focused on close cooperation between the agencies. The agreement enables the ISA to draw upon the UN for facilities and services as may be required.75782baa0f0a This mandate to collaborate could be employed towards institutional strengthening, noting the various accountability and oversight mechanisms housed within the UN that are currently lacking at the ISA.

4. Pathways for implementation

Anti-corruption interventions must be fit-for-context, and will work best when integrated into broader reforms.d0b94614649f Whilst there are some aspects of the ISA’s institutional set-up that are intrinsic and difficult to change, there are many achievable measures that the ISA could take to reduce corruption risks and manage conflicts, and stringent penalties should conflicts of interest be uncovered.

Political will

Political leadership will be needed to address corruption risks at the ISA. Member states need to affect an organisational culture to shift towards championing institutional reform rather than deflecting criticism or ‘good governance façades’.954a5f906cc9 In practice, this means the Assembly and the Council signalling publicly its intention to adopt a programme of reform. This should include endorsing a plan of work to develop the necessary administrative policies and functions to ensure probity and oversight mechanisms and initiating transparent and impartial investigations into any existing allegation of misconduct. Establishment of a dedicated oversight committee for this process may help ensure progress and accountability. Support from independent experts may assist to challenge entrenched practices that undermine the ISA’s credibility.

A programme of reform

Due process in developing a programme of reform is also important. The overdue periodic review of the ISA’s functioning required by Article 154 of UNCLOS, presents a critical opportunity for the ISA to confront institutional weaknesses and restore credibility. By conducting a transparent, inclusive, and evidence-based assessment of its operations, using independent reviewers and public consultations, the ISA can identify governance gaps, evaluate the uptake of past recommendations, and develop a concrete roadmap for reform. That roadmap can be worked into the ISA’s next strategic plan. Use of SMART47c8159d4cfe objectives and clear allocation of responsibilities (and monitoring and follow-up if duties are not discharged) can help to strengthen oversight and accountability and build the ISA’s anti-corruption resilience before exploitation activities scale up. This should also be an ongoing process, with regular monitoring, evaluation and learning from anti-corruption interventions. Recognising the ISA’s duty of cost-effectiveness,81a41587374c the ISA can evaluate each measure against agreed criteria such as risk assessment, feasibility, effectiveness, legitimacy, proportionality, and alignment with UNCLOS. This should enable identification and prioritisation of systems, personnel, or decisions most at risk of undue pressure.

Cooperation with other multilaterals

Collaboration is also essential. No IGO is an island; even one that manages the remotest locations on Earth! The ISA has multitudinous stakeholders with a shared objective towards good governance. The ISA is also just one in a framework of different multilateral bodies and processes, with overlapping membership. For ocean governance alone, there are the following:

- Food and Agriculture Organization

- United Nations Division for Ocean Affairs and the Law of the Sea (UNDOALOS)

- United Nations Environment Programme

- International Maritime Organization

- Regional Seas Programmes (including the Convention for the Protection of the Marine Environment of the North-East Atlantic (OSPAR))

- Commission for the Conservation of Antarctic Marine Living Resources

- Convention on the Conservation of Migratory Species of Wild Animals

- International Whaling Commission

- 17 regional fisheries management organisations

- Biodiversity Beyond National Jurisdiction bodies under development

This brings opportunities for coalition-building, mutual support, and alignment with other intergovernmental agencies. Harmonisation and integration between the rules of the ISA and of other organisations would also bring user-friendly benefits to member states and other stakeholders who engage across different agencies and processes.

5. A path to legitimacy

As noted by a recent ISA commentator, ‘reform is not delay – it is the only path to legitimacy’.aee53c4f67e5 The stakes at the ISA are high. A failure to address some of the governance gaps addressed in this paper would lead to high-profile failure and potentially a significant loss to humankind in the form of mineral assets, optimal economic gain, technical transfer, and/or environmental harm on a global scale. If lower-income countries bear the brunt, this would only add to historic inequalities, rather than address them.

Integrity in the ISA’s governance is foundational to the legitimacy, sustainability, and effectiveness of its regulatory regime. This organisation acts on behalf of us all and holds in its power half of the planet’s surface. Yet the ISA faces documented and growing risks of conflict of interest, corruption, and regulatory capture – without a current roadmap for reform. This places at risk both the common heritage and the marine environment.

In a world of geopolitical fragmentation, the ISA has an opportunity to showcase successful multilateralism. This will require political leadership and institutional reform now. Whilst UNCLOS to some degree embeds conflicts of interest risk in the ISA’s structure and mandate, there are many measures – not currently taken – that could help to manage risk. The opportunity for member states, ISA personnel, and other stakeholders to act decisively is now: to establish independent oversight mechanisms, enforce procedural safeguards, and ensure that governance structures are resilient against undue influence. Proactive reinforcement of the ISA’s integrity is urgently required before exploitation begins and not after irreparable harm is done.

6. Recommendations for the International Seabed Authority and its state membership

1. Strengthen governance and oversight

- Establish a state-led oversight body with regular meetings, accountable to the Assembly, acting as a ‘critical friend’ to review ISA governance and performance.

- Institute periodic reviews of rules of procedure for all ISA organs, focusing on inclusivity, transparency, and conflict of interest safeguards.

- Create clear policy regarding the respective roles and accountabilities of the different ISA organs and ensure mandates from the Assembly and Council for any responsibilities assigned to subsidiary organs beyond UNCLOS provisions.

- Require bi-annual reports from the Secretariat to member states on financial management, personnel conduct, and administrative decisions.

2. Improve transparency and access to information

- Publish detailed reports of LTC, Finance Committee, Council, and Assembly meetings, and post audio recordings online for a set period before archiving in the ISA library.

- Establish procedures that allow observers to attend LTC and Finance Committee’s annual meetings, reserving confidential agenda items as exceptions.

- Establish open-contracting principles: publishing tenders, winning bids, contract values, and progress updates; disclose procurement rules and selection criteria for consultants and suppliers.

- Develop an open-access data management policy including publication of ISA contracts and contractor performance reports.

- Explain and review confidentiality classifications and NDAs against best practices for intergovernmental organisations, prioritising transparency.

3. Enhance institutional integrity and compliance

- Create an internal compliance function within the Secretariat to monitor adherence to institutional policies, codes of conduct, and conflict of interest disclosures.

- Operationalise integrity measures for the Enterprise based on OECD guidelines for state-owned enterprises and anti-corruption frameworks.

- Establish a trained compliance and enforcement division to regulate ISA contractors.

- Integrate anti-corruption indicators into ISA’s performance and reporting framework.

- Require the ISA to undergo independent financial audits with expanded scope beyond annual accounts to include internal financial processes, reporting to the Finance Committee.

4. Manage conflicts of interest

- Create a conflict-of-interest registry for ISA organs and contractors, including public disclosure of interests, gifts, meetings, and expenditures above a threshold.

- Establish a beneficial ownership registry for contractors.

- Implement a ‘cooling-off’ period for ISA staff moving to contractor roles and vice versa (minimum 12 months), linking compliance to eligibility for ISA contracts.

- Develop a code of conduct for staff and committee members with enforcement mechanisms overseen by the internal compliance entity.

5. Promote participation and inclusivity

- Boost member state engagement through virtual participation options, funding for in-person attendance, and capacity-building programmes to increase political buy-in.

- Standardise public consultation procedures and protect the rights of civil society, media, and environmental human rights defenders in ISA processes.

- Agree on and apply transparent rules for selection of participants in ISA working groups and workshops.

6. Ensure accountability and remedies

- Establish an independent ombudsperson to manage complaints and extend whistleblower protections to contractor employees and subcontractors, or other complainants who may fear victimisation and reprisals.

- Create an administrative appeal mechanism for reviewing specific ISA decisions, with clear rules on scope, standing, and procedure.

- Determine clear rules for penalties in cases of contractor non-compliance with anti-corruption rules.

7. Conduct strategic review

- Include conflict of interest and corruption risk assessment in the ISA’s periodic strategic reviews under Article 154.

- Publish findings in relation to conflict of interest and corruption risk arising from the ISA’s strategic review in a short briefing with recommendations and establish an Assembly working group to oversee implementation.

- Establish ISA reporting metrics on conflict of interest and corruption management.

8. Apply requirements to ISA contractors

- Require reporting to the ISA’s beneficial ownership register and conflict of interest register.

- Require reporting of each contractor’s full subcontracting chains and corporate groups.

- Demonstrate implementation of an effective anti-bribery management system and link adherence to eligibility for ISA tenders.

- For background information on the ISA and deep seabed mining, please see ISA 2025c; Kröger et al 2025; and UN 2025.

- Articles 1(1) of UNCLOS; ISA (2025c); and Lodge (2020).

- Part XI, Articles 136, 140, 145 and 153 of UNCLOS (1982).

- Articles 143, 153, 160 and 162 of UNCLOS. For information on development of the Mining Code for Exploitation, see ISA 2025f.

- Some sources suggest that the deep seabed sediment is also a fourth potential resource, containing rare earth elements.

- The designation of the deep seabed as the common heritage of humankind under UNCLOS establishes that its mineral resources are collectively owned by present and future generations, with benefits to be shared equitably (including intergenerationally). The ISA is mandated to manage the minerals, and no state or entity may unilaterally appropriate or claim sovereign rights over them. Originating in the 1960s through proposals led by Malta’s Ambassador Arvid Pardo, the principle seeks to prevent both the ‘tragedy of the commons’ and patterns of colonial extractivism. Comparable designations apply to the moon and outer space.

- Amon et al. 2022; Levin et al. 2020.

- For details of ISA-issued deep seabed minerals contracts, see ISA 2025b. For details of countries who have declared moratorium or ‘precautionary pause’ positions on deep seabed mining, see DSCC 2025.

- See Office of the President of the United States 2025. For a statement in response from ISA Secretary-General, see de Carvalho 2025b.

- See TMC 2025; and Hutchins 2025. For legal analysis of the TMC US application, see Fisher and Robb 2025.

- The distinction between internal and external criticism is not clear-cut as ISA delegates, who are quoted by the media, include academics who may publish externally, and ISA deliberations may include experts, who may be considered as external, as observers.

- For instance, Delacroix 2024; Lipton 2022; 2024; McVeigh 2023; Woody 2021; and Woody and Halper 2022.

- This report does not examine specific cases of conflict of interest because its purpose is to highlight the potential for such conflicts and propose practical measures to strengthen the ISA, rather than focus on past shortcomings. To see examples of media reporting on these issues, see the previous footnote.

- ISA 2024.

- Drawn from Kolstad et al. 2008; Williams and Dupuy 2016; and Libert and Brillaud 2016.

- Ibid.

- DSCC 2024, 2; Chene 2010; Gillies 2009.

- OECD n.d.

- OECD et al. 2020.

- Council of Europe 2000.

- UNCAC 2003, Articles 7(4), 8(5) and 12(2). The UNCAC identifies the following forms of corruption: bribery and embezzlement in the public sector; bribery and embezzlement in the private sector; trading in influence; abuse of functions; illicit enrichment; money-laundering; concealment; and obstruction of justice. ISA members that have not ratified UNCAC are limited to St Vincent and Grenadines, and Monaco. States outside of UNCAC and UNCLOS are Andorra, Eritrea, North Korea, and Syria.

- Dobush and Warner 2024;Vescovo 2025.

- Pickens et al. 2024.

- Williams 2019, 1.

- Craik et al. 2025; Collins and French 2020.

- The following analysis of governance vulnerabilities at the ISA are drawn from these collectively cited papers: Seascape Consultants 2016; Ardron et al. 2018; Collins and French 2020; Komaki and Fluharty 2020; Morgera and Lily 2022; Ardron et al. 2023; Bosco et al. 2023; Deberdt and James 2024; Lily and Chakraborty 2025; Garcia-Soto 2025; Alger et al. 2025; Craik et al. 2025.

- While competing mandates are common within states (eg promoting economic growth while protecting the environment), states typically distribute these functions across separate institutions with distinct lines of accountability, political oversight, and judicial review. By contrast, the ISA concentrates both the extractive and environmental protection mandates within a single international organisation that lacks the internal separation of powers, democratic checks, and domestic accountability mechanisms available to states. This institutional design means that mandate‑level tensions are not merely analogous to those within states: they are structurally amplified, because the same organs, even the same individuals, are responsible for advancing potentially conflicting objectives. The ISA also lacks some of the corrective mechanisms (elections, parliamentary scrutiny, administrative courts) that help states manage such tensions.

- Collins and French 2020.

- The Council reserved Areas of Particular Environmental Interest covering 1.97 km2 million in an area of the Clarion-Clipperton Zone at the recommendation of the Council. Exploration areas cover 1.2 km2. These zones were not envisioned in UNCLOS, they were decided upon after the majority of the exploration contracts were awarded and have been criticised for their lack of ecological representativity as they are arranged around potential mining areas. Areas of Interest would be left intact for 5 years and renewed continually unless ISA bodies decide otherwise.

- An issue that remains on the ISA’s agenda for discussion is the Finance Committee’s proposal that the first mining revenue could be used to reimburse the fees paid by the states who are the largest contributors to the ISA.

- Article 161(8)(d)–(g) of UNCLOS, and section 3(2) and (3) of the Annex to the ‘Agreement Relating to the Implementation of Part XI of UNCLOS' (1994).

- The Council has never voted; the Assembly has only held secretary-general elections and once in 1998, the Assembly voted on a budgetary matter on state contributions. See Lodge 2020.

- While the ISA includes both pro‑ and anti‑mining factions, the balance of influence between them remains uncertain. Advocacy dynamics are also uneven. Industry actors typically have far greater resources than civil society organisations, but deep seabed mining is a new and emerging industry yet to generate revenue. The Council’s chamber structure does give greater weight to states with commercial interests in deep seabed mining, which could tilt decision‑making toward pro‑mining positions.

- Section 3 paragraphs (9) and (15) of the Annex to the ‘Agreement Relating to the Implementation of Part XI of UNCLOS’ (1994).

- China, Czech Republic, France, Germany, India, Jamaica, Japan, Russian Federation, United Kingdom of Great Britain, Northern Ireland.

- See list of presidents of the council and

people at the Interoceanmetal Joint Organisation. - Jamaica, whose nationals were formally President of Assembly, and Chair of the LTC, and who stepped in to cover a last-minute absence of Council Presidency.

- NRGI 2014, p. 10–11.

- Lily and Chakraborty 2025.

- Bosco et al. 2023.

- ISA 2025a.

- ISA 2025d.

- ISA 2021.

- Annex, section 7(1) of Agreement Relating to the Implementation of Part XI of UNCLOS’ (1994).

- Annex, section 1(3) of Agreement Relating to the Implementation of Part XI of UNCLOS’ (1994).

- For commentary about risks associated with the ISA handling fund management in-house, please see section 4 of this article: Wilde et al. 2023.

- Morgera and Lily 2022.

- Article 163(8) of UNCLOS.

- See ISA 2025e. The LTC members, for example, from Germany, Korea, and Japan all list institutions that hold current ISA exploration contracts as their employers.

- Lily and Chakraborty 2025.

- Deberdt and James 2024.

- In addition to the academic sources cited, the importance of whistle-blowing and current gaps in the ISA framework are discussed in Kohn 2024.

- Article 154 of UNCLOS.

- NRGI 2014, p. 7–9.

- For instance, de Carvalho 2025a.

- See U4 2021.

- Article 162 of UNCLOS.

- Wood 1999.

- Williams and Dupuy 2016.

- Williams 2019.

- Abbreviation for goals that are strategic, measurable, achievable/attainable, relevant/realistic, and time-bound.

- Annex, Section 1(2) of Agreement Relating to the Implementation of Part XI of UNCLOS’ (1994).

- Garcia-Soto 2025, p. 9.